library(tidyverse)

library(tidyquant)

library(patchwork)

library(scales)

library(writexl)

library(zoo)

library(moments)

library(rugarch); library(broom)

library(gt)Contents

- Volatility as annualized standard deviation

- Varies by frequency (periodicity) and window

- Exponentially weighted moving average (EWMA)

- GARCH(1,1)

- The actual returns are non-normal (heavy-tailed)

Load packages

Volatility as annualized standard deviation

Retrieve prices, calculate log returns and create all_returns_* dataframe

# symbols <- c("PG", "JPM", "NVDA")

# mult_stocks <- tq_get(symbols, get = "stock.prices", from = "2010-12-31", to = "2023-11-09")

# mult_stocks$symbol <- mult_stocks$symbol <- factor(mult_stocks$symbol, levels = c("PG", "JPM", "NVDA"))

# saveRDS(mult_stocks, "mult_stocks.rds")

mult_stocks <- readRDS("mult_stocks.rds")

# tq_mutate_fun_options() returns list of compatible mutate functions by pkg

calculate_returns <- function(data, period) {

data |>

group_by(symbol) |>

tq_transmute(select = adjusted,

mutate_fun = periodReturn,

period = period,

type = "log")

}

periods <- c("daily", "weekly", "monthly", "quarterly", "yearly")

# all_returns_daily <- calculate_returns(mult_stocks, "daily")

# all_returns_weekly <- calculate_returns(mult_stocks, "weekly")

# all_returns_monthly <- calculate_returns(mult_stocks, "monthly")

# all_returns_quarterly <- calculate_returns(mult_stocks, "quarterly")

all_returns <- set_names(periods) |> map(~ calculate_returns(mult_stocks, .x))

all_returns <- map(all_returns, ~ .x %>%

group_by(symbol) %>%

arrange(date) %>% # Sort by date within each group

slice(-1) %>% # Remove the first row for each group

ungroup())

all_returns_daily <- all_returns$daily

all_returns_weekly <- all_returns$weekly

all_returns_quarterly <- all_returns$quarterly

all_returns_monthly <- all_returns$monthlySave to Excel (to manually check calcualtions). But after first time, eval = FALSE

write_xlsx(all_returns, path = "all_returns.xlsx")

# This assumes 'all_returns' is a named list of data frames

# and each data frame has a 'symbol' column for stock tickers

# Step 1: Split each data frame by 'symbol' and create a named list of data frames

all_returns_by_stock <- map(all_returns, function(df) {

split(df, df$symbol)

})

# Step 2: Name each data frame according to the period and stock

all_returns_by_stock <- imap(all_returns_by_stock, function(df_list, period_name) {

set_names(df_list, paste(period_name, names(df_list), sep = "_"))

})

# Flatten the list of lists into a single list of data frames

all_returns_by_stock_flat <- flatten(all_returns_by_stock)

# Step 3 and 4: Write the list of data frames to an Excel file

write_xlsx(all_returns_by_stock_flat, path = "all_returns_by_stock.xlsx")Different frequencies but the same (four year) window

calc_rolling_sd <- function(data, return_col_name, window_width) {

data |>

group_by(symbol) |>

mutate(rolling_sd = rollapply(get(return_col_name),

width = window_width,

FUN = sd,

align = "right", fill = NA)) |>

ungroup()

}

# Window lengths for each frequency (aka, periodicity)

W.daily <- 250 * 4

W.weekly <- 52 * 4

W.monthly <- 12 * 4

W.quarterly <- 4 * 4

all_returns_daily <- calc_rolling_sd(all_returns_daily, "daily.returns", W.daily)

all_returns_weekly <- calc_rolling_sd(all_returns_weekly, "weekly.returns", W.weekly)

all_returns_monthly <- calc_rolling_sd(all_returns_monthly, "monthly.returns", W.monthly)

all_returns_quarterly <- calc_rolling_sd(all_returns_quarterly, "quarterly.returns", W.quarterly)Still different frequencies (aka, periodicity) but annualized

# Function to calculate annualized volatility and add frequency

calc_annualized_vol <- function(df, sd_col, periods_per_year, freq_label) {

df |>

mutate(

annualized_vol = !!rlang::sym(sd_col) * sqrt(periods_per_year),

frequency = freq_label

)

}

# Calculate annualized volatility for each dataframe EXCEPT Quarterly

all_returns_daily <- calc_annualized_vol(all_returns_daily, "rolling_sd", 252, "Daily")

all_returns_weekly <- calc_annualized_vol(all_returns_weekly, "rolling_sd", 52, "Weekly")

all_returns_monthly <- calc_annualized_vol(all_returns_monthly, "rolling_sd", 12, "Monthly")

# Combine the data frames into one

all_returns_combined <- bind_rows(all_returns_daily, all_returns_weekly, all_returns_monthly)

all_returns_combined <- all_returns_combined |>

mutate(frequency = factor(frequency, levels = c("Daily", "Weekly", "Monthly")))

# Plot the combined data with ggplot2

color_pg <- "chartreuse2" # don't end up using these

color_jpm <- "dodgerblue2"

color_nvda <- "coral1"

color_tenor1 <- "khaki3"

color_tenor2 <- "coral"

color_tenor3 <- "lightseagreen"

color_tenor4 <- "slateblue"

custom_colors <- c("Daily" = color_tenor1, "Weekly" = color_tenor2, "Monthly" = color_tenor3)

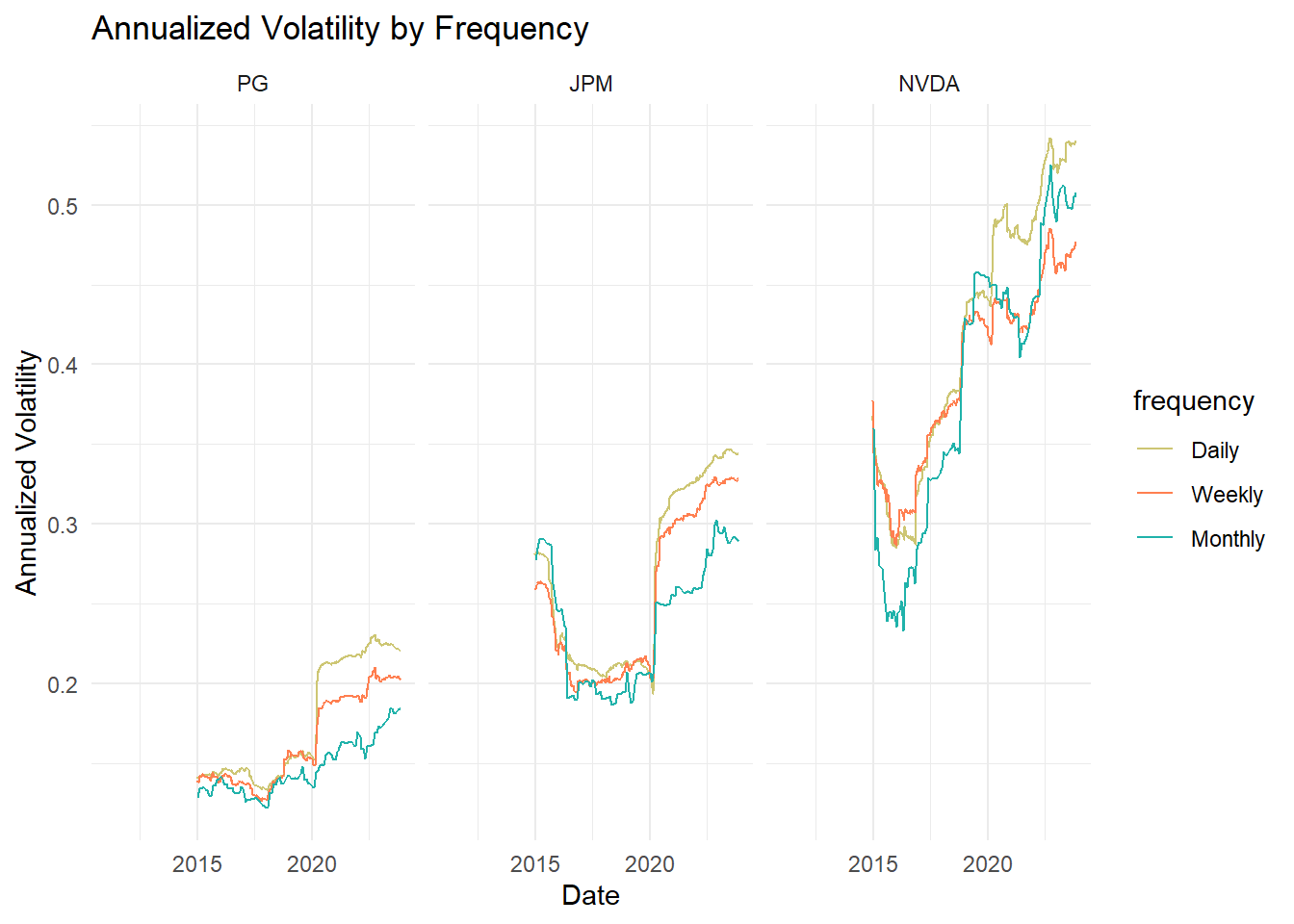

all_returns_combined |> ggplot(aes(x = date, y = annualized_vol,

color = frequency,

group = interaction(symbol, frequency))) +

geom_line() +

labs(title = "Annualized Volatility by Frequency",

x = "Date",

y = "Annualized Volatility") +

theme_minimal() +

scale_color_manual(values = custom_colors) +

facet_wrap(~symbol)

# mean annualized vol by symbol and frequency

all_returns_combined |>

group_by(symbol, frequency) |>

summarize(annualized_vol = mean(annualized_vol, na.rm = TRUE)) |>

pivot_wider(names_from = frequency, values_from = annualized_vol) |>

arrange(Daily)# A tibble: 3 × 4

# Groups: symbol [3]

symbol Daily Weekly Monthly

<fct> <dbl> <dbl> <dbl>

1 PG 0.176 0.164 0.147

2 JPM 0.265 0.255 0.239

3 NVDA 0.421 0.396 0.388Different windows but same (DAILY) frequency

# colors from my var article

# col_ticker_fills <- c("PG" = "chartreuse2", "JPM" = "dodgerblue2", "NVDA" = "coral1")

windows <- c(20, 90, 250, 500)

# parse into per-ticker df and delete rolling_sd column from prior

pg_data <- all_returns_daily |> filter(symbol == "PG") |> select(!rolling_sd)

jpm_data <- all_returns_daily |> filter(symbol == "JPM") |> select(!rolling_sd)

nvda_data <- all_returns_daily |> filter(symbol == "NVDA") |> select(!rolling_sd)

# Specify your window sizes directly in the loop

for (w in windows) {

pg_data <- pg_data |>

mutate(!!paste0("rolling_sd_", w) := rollapply(daily.returns,

width = w,

FUN = sd,

align = "right", fill = NA))

jpm_data <- jpm_data |>

mutate(!!paste0("rolling_sd_", w) := rollapply(daily.returns,

width = w,

FUN = sd,

align = "right", fill = NA))

nvda_data <- nvda_data |>

mutate(!!paste0("rolling_sd_", w) := rollapply(daily.returns,

width = w,

FUN = sd,

align = "right", fill = NA))

}

plot_rolling_sd <- function(data, stock_name, ylim, custom_colors, custom_alphas) {

# Assume data has columns 'date', and rolling_sd_* where * is the window size

rolling_sd_long <- data |>

pivot_longer(cols = starts_with("rolling_sd_"), names_to = "window", values_to = "rolling_sd")

desired_order <- c("rolling_sd_20", "rolling_sd_90", "rolling_sd_250", "rolling_sd_500")

rolling_sd_long$window <- factor(rolling_sd_long$window, levels = desired_order)

ggplot(rolling_sd_long, aes(x = date, y = rolling_sd, color = window)) +

geom_line(aes(alpha = window)) +

scale_color_manual(values = custom_colors) +

scale_alpha_manual(values = custom_alphas) +

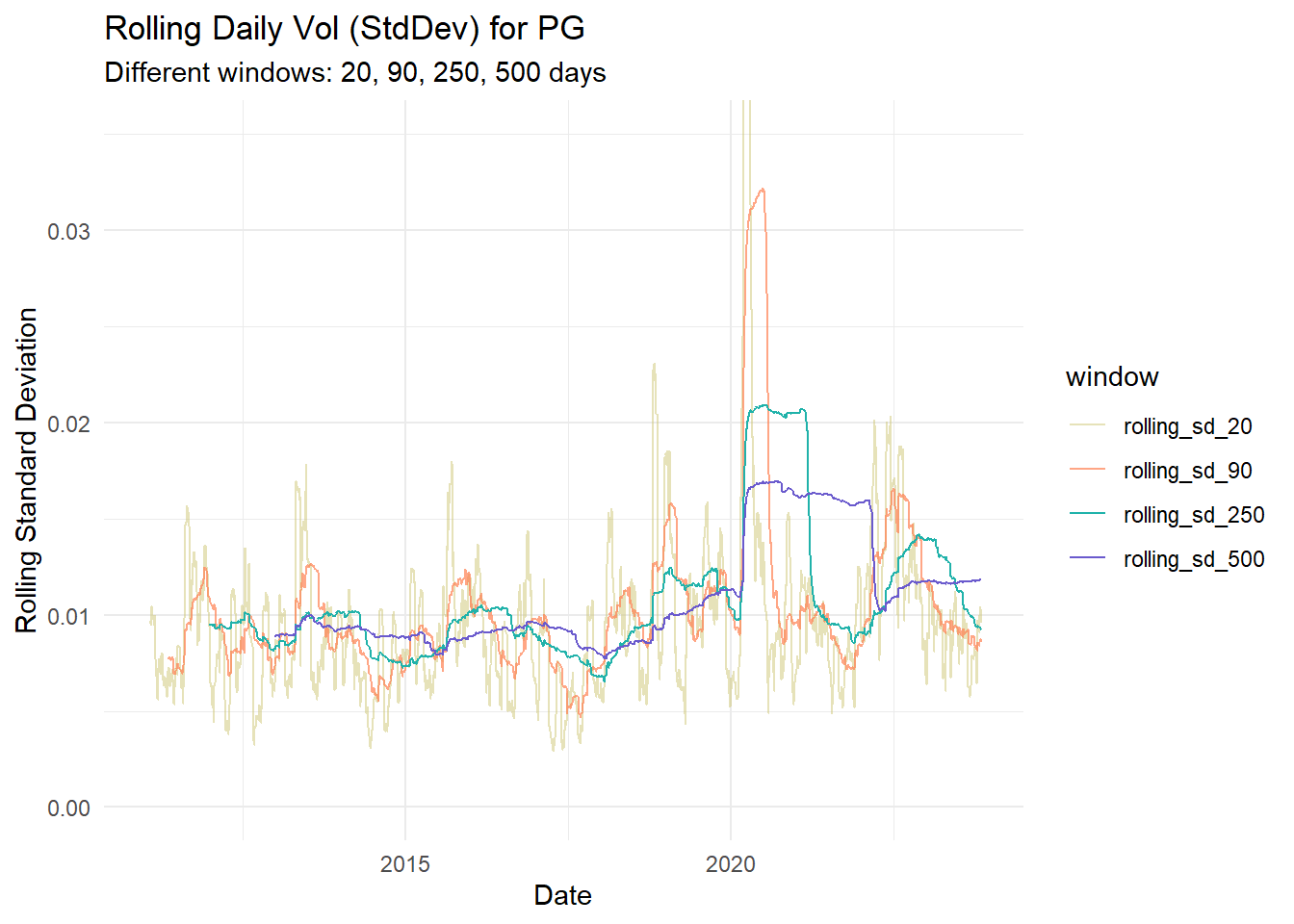

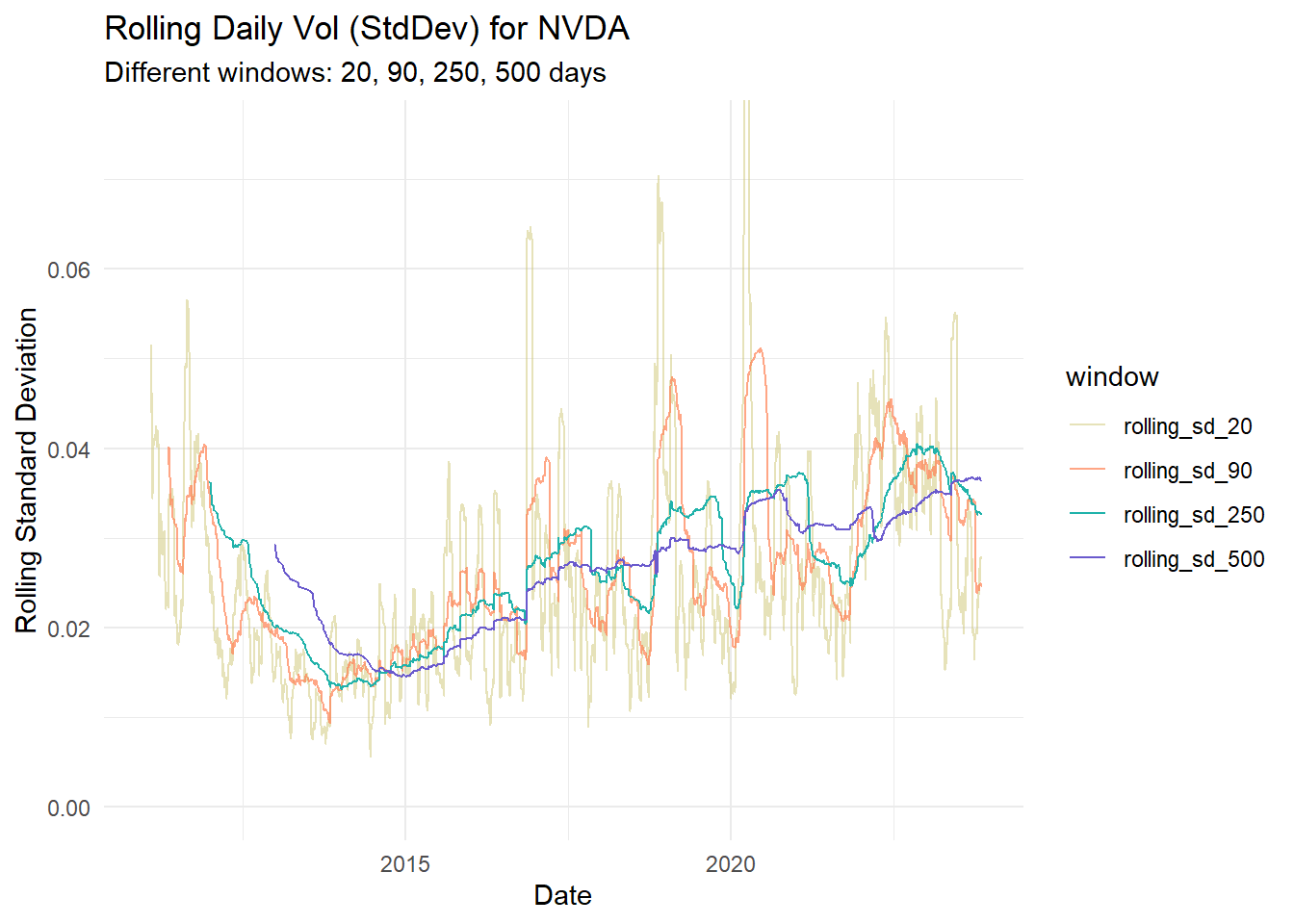

labs(title = paste("Rolling Daily Vol (StdDev) for", stock_name),

subtitle = paste("Different windows:", paste(windows, collapse = ", "), "days"),

x = "Date",

y = "Rolling Standard Deviation") +

theme_minimal() +

coord_cartesian(ylim = ylim) +

theme(legend.position = "right")

}

# custom_colors <- c("rolling_sd_20" = "firebrick1",

# "rolling_sd_90" = "royalblue",

# "rolling_sd_250" = "springgreen4",

# "rolling_sd_500" = "darkorange")

custom_colors <- c("rolling_sd_20" = color_tenor1,

"rolling_sd_90" = color_tenor2,

"rolling_sd_250" = color_tenor3,

"rolling_sd_500" = color_tenor4)

custom_alphas <- c("rolling_sd_20" = 0.5,

"rolling_sd_90" = 0.7,

"rolling_sd_250" = 1.0,

"rolling_sd_500" = 1.0)

pg_roll_plot <- plot_rolling_sd(pg_data, "PG", c(0, 0.0350), custom_colors, custom_alphas)

jpm_roll_plot <- plot_rolling_sd(jpm_data, "JPM", c(0, 0.0550), custom_colors, custom_alphas)

nvda_roll_plot <- plot_rolling_sd(nvda_data, "NVDA", c(0, 0.0750), custom_colors, custom_alphas)

pg_roll_plot

jpm_roll_plot

nvda_roll_plot

# Function to summarize and extract the most recent rolling standard deviations

summarize_and_extract_recent_sd <- function(data) {

summarized <- data %>%

summarize(

mean_sd_20 = mean(rolling_sd_20, na.rm = TRUE),

mean_sd_90 = mean(rolling_sd_90, na.rm = TRUE),

mean_sd_250 = mean(rolling_sd_250, na.rm = TRUE),

mean_sd_500 = mean(rolling_sd_500, na.rm = TRUE)

)

most_recent <- data %>%

slice(n()) %>%

select(rolling_sd_20, rolling_sd_90, rolling_sd_250, rolling_sd_500) %>%

rename(recent_sd_20 = rolling_sd_20,

recent_sd_90 = rolling_sd_90,

recent_sd_250 = rolling_sd_250,

recent_sd_500 = rolling_sd_500)

bind_cols(summarized, most_recent)

}

# Apply the function to each data frame and bind rows into a single tibble

summary_tibble <- bind_rows(

pg = summarize_and_extract_recent_sd(pg_data),

jpm = summarize_and_extract_recent_sd(jpm_data),

nvda = summarize_and_extract_recent_sd(nvda_data),

.id = "stock"

)

summary_tibble |>

gt() |>

tab_header(

title = "Rolling daily volatility"

) |>

cols_label(

mean_sd_20 = "20",

mean_sd_90 = "90",

mean_sd_250 = "250",

mean_sd_500 = "500",

recent_sd_20 = "20",

recent_sd_90 = "90",

recent_sd_250 = "250",

recent_sd_500 = "500"

) |>

fmt_percent(columns = 2:9,

rows = everything()) |>

tab_spanner(

label = "Mean",

columns = 2:5

) |>

tab_spanner(

label = "Most recent (2023-11-08)",

columns = 6:9

) |>

cols_width(

mean_sd_20 ~ px(80),

recent_sd_20 ~ px(80)

) |>

data_color(

columns = 6:9,

rows = 3,

method = "numeric",

domain = c(0.02, 0.04),

palette = c("lightcyan", "lightcyan3")

)| Rolling daily volatility | ||||||||

|---|---|---|---|---|---|---|---|---|

| stock | Mean | Most recent (2023-11-08) | ||||||

| 20 | 90 | 250 | 500 | 20 | 90 | 250 | 500 | |

| pg | 0.98% | 1.03% | 1.07% | 1.09% | 0.96% | 0.86% | 0.93% | 1.18% |

| jpm | 1.53% | 1.61% | 1.66% | 1.66% | 1.26% | 1.01% | 1.36% | 1.64% |

| nvda | 2.54% | 2.64% | 2.66% | 2.64% | 2.76% | 2.47% | 3.25% | 3.63% |

# GPT wrote this routine to summarize!

summarize_rolling_sd <- function(data) {

# Define the desired order for the window sizes

window_order <- c("rolling_sd_20", "rolling_sd_90", "rolling_sd_250", "rolling_sd_500")

summarized_data <- data %>%

summarize(across(starts_with("rolling_sd_"), mean, na.rm = TRUE)) %>%

pivot_longer(cols = everything(), names_to = "window", values_to = "rolling_sd") %>%

mutate(window = factor(window, levels = window_order)) %>%

arrange(window)

return(summarized_data)

}

# Apply the summarize function to each stock and combine into a single tibble

all_summaries <- bind_rows(

pg = summarize_rolling_sd(pg_data),

jpm = summarize_rolling_sd(jpm_data),

nvda = summarize_rolling_sd(nvda_data),

.id = "stock"

)

# Print the combined summarized data

print(all_summaries)# A tibble: 12 × 3

stock window rolling_sd

<chr> <fct> <dbl>

1 pg rolling_sd_20 0.00977

2 pg rolling_sd_90 0.0103

3 pg rolling_sd_250 0.0107

4 pg rolling_sd_500 0.0109

5 jpm rolling_sd_20 0.0153

6 jpm rolling_sd_90 0.0161

7 jpm rolling_sd_250 0.0166

8 jpm rolling_sd_500 0.0166

9 nvda rolling_sd_20 0.0254

10 nvda rolling_sd_90 0.0264

11 nvda rolling_sd_250 0.0266

12 nvda rolling_sd_500 0.0264 Exponentially weighted moving average (EWMA)

# Function to calculate EWMA variance

calculate_ewma_variance <- function(returns, lambda, W) {

ewma_var <- rep(NA, length(returns))

ewma_var[W] <- var(returns[1:W]) # Initialize the first EWMA variance

for (i in (W+1):length(returns)) {

# Using the EWMA formula

ewma_var[i] <- lambda * ewma_var[i-1] + (1 - lambda) * returns[i]^2

}

return(ewma_var)

}

# Example lambda value

W <- 250

lambda <- 0.94

# Use rollapply with your custom EWMA function

# Assuming the 'returns' column in all_returns_daily is the daily return for each stock

all_returns_daily <- all_returns_daily |>

group_by(symbol) |>

mutate(ewma_variance = calculate_ewma_variance(daily.returns, lambda, W)) |>

ungroup()

# Calculate the EWMA volatility from the EWMA variance

all_returns_daily <- all_returns_daily |>

mutate(ewma_sd = sqrt(ewma_variance))

# Reshape the data to long format for ggplot2

all_returns_long <- all_returns_daily |>

pivot_longer(cols = c("rolling_sd", "ewma_sd"),

names_to = "sd_type",

values_to = "sd_value")

# Plot the data with ggplot2

custom_sd_colors <- c("rolling_sd" = color_tenor4, "ewma_sd" = color_tenor2)

all_returns_long |> ggplot (aes(x = date, y = sd_value, color = sd_type)) +

geom_line(aes(alpha = sd_type)) +

scale_color_manual(values = custom_sd_colors) +

scale_alpha_manual(values = c(0.5, 1.0)) +

labs(title = "EWMA is much more reactive than unweighted StdDev",

subtitle = "(rolling_sd window = 250 days * 4 years = 1000 days)",

x = "Date",

y = "Standard Deviation") +

facet_wrap(~symbol) +

coord_cartesian(ylim = c(0, 0.050)) +

theme_minimal() +

theme(legend.position = "bottom")

Let’s compare different lambda (aka, smoothing) parameters

library(dplyr)

library(ggplot2)

library(tidyr)

plot_ewma_for_stock <- function(data, symbol, returns_col, lambda_list,

custom_colors, custom_alphas, ylim) {

# Function to calculate EWMA variance - make sure this is defined in your environment

calculate_and_store_ewma <- function(data, symbol, returns_col, lambda_list) {

for (lambda in lambda_list) {

W = 250

lambda <- lambda

ewma_col_name <- paste0("lambda_", as.character(lambda))

data <- data |>

mutate(

!!ewma_col_name := sqrt(calculate_ewma_variance(get(returns_col), lambda, W))

)

}

return(data)

}

# Calculate and store EWMA with multiple parameters for the specified stock

stock_ewma <- calculate_and_store_ewma(data, symbol, returns_col, lambda_list)

# Pivot the data to long format for plotting

stock_ewma_long <- stock_ewma |>

pivot_longer(cols = starts_with("lambda"), names_to = "lambda", values_to = "ewma_sd")

# Plot the EWMA standard deviations for different parameter sets

gg <- ggplot(stock_ewma_long, aes(x = date, y = ewma_sd, color = lambda)) +

geom_line(aes(alpha = lambda)) +

scale_color_manual(values = custom_colors) +

scale_alpha_manual(values = custom_alphas) +

labs(title = paste("EWMA volatility for", symbol, "with Different Parameters"),

x = "Date",

y = "EWMA Standard Deviation") +

coord_cartesian(ylim = c(0, ylim)) +

theme_minimal() +

theme(legend.position = "right")

return(gg)

}

# Define the sets of parameters you want to compare

lambda_list <- c(0.91, 0.94, 0.97)

# custom_colors <- c("lambda_0.91" = "firebrick1",

# "lambda_0.94" = "royalblue",

# "lambda_0.97" = "springgreen4")

custom_colors <- c("lambda_0.91" = color_tenor1,

"lambda_0.94" = color_tenor2,

"lambda_0.97" = color_tenor4)

custom_alphas <- c("lambda_0.91" = 0.6,

"lambda_0.94" = 0.8,

"lambda_0.97" = 1.0)

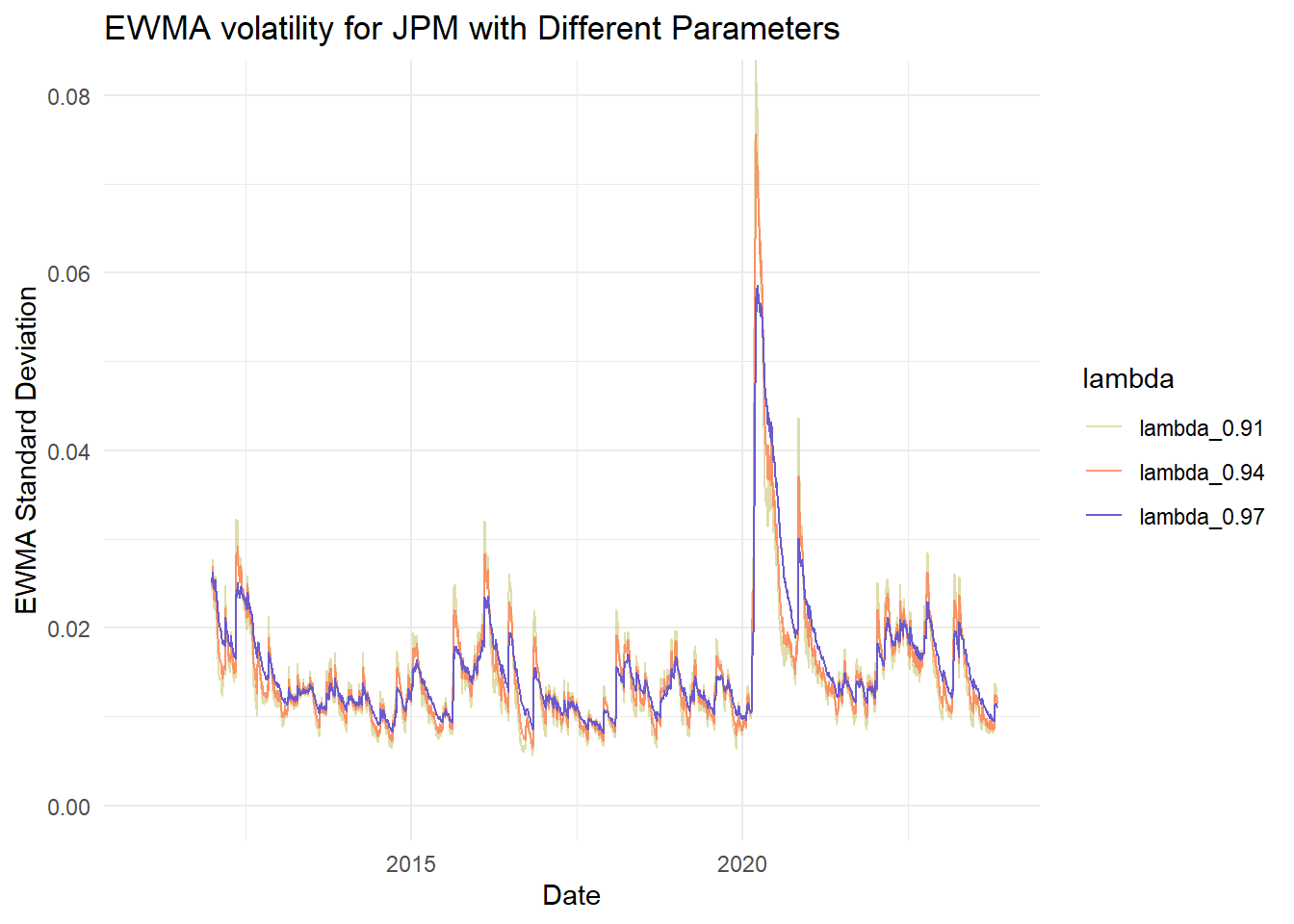

jpm_ewma_plot <- plot_ewma_for_stock(jpm_data, "JPM", "daily.returns", lambda_list,

custom_colors, custom_alphas, 0.080)

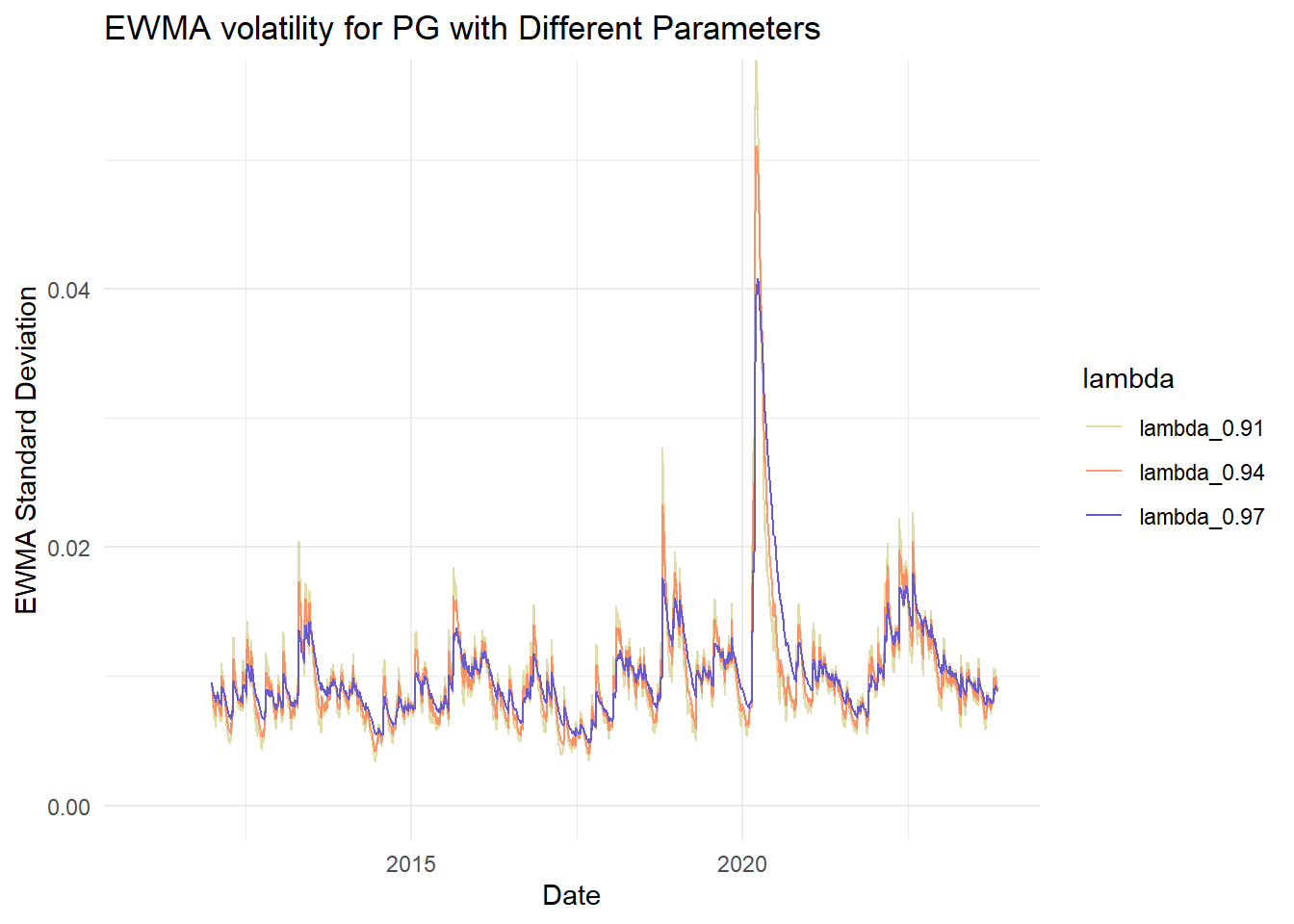

pg_ewma_plot <- plot_ewma_for_stock(pg_data, "PG", "daily.returns", lambda_list,

custom_colors, custom_alphas, 0.0550)

nvda_ewma_plot <- plot_ewma_for_stock(nvda_data, "NVDA", "daily.returns", lambda_list,

custom_colors, custom_alphas, 0.070)

jpm_ewma_plot

pg_ewma_plot

nvda_ewma_plot

GARCH(1,1)

Fitting the parameters

# library(rugarch)

# Define the GARCH(1,1) specification outside the loop to avoid redundancy

spec <- ugarchspec(variance.model = list(model = "sGARCH", garchOrder = c(1, 1)),

mean.model = list(armaOrder = c(0, 0), include.mean = TRUE),

distribution.model = "norm")

# Fit the GARCH(1,1) model for each stock symbol

garch_models <- all_returns_daily |>

group_by(symbol) |>

nest() |>

mutate(model = map(data, ~ ugarchfit(spec, data = .$daily.returns)))

# Manual extraction of coefficients

garch_coef_manual <- garch_models |>

mutate(coef = map(model, function(m) as.data.frame(t(coef(m))))) |>

select(symbol, coef) |>

unnest(coef)

garch_coef_manual <- garch_coef_manual |> ungroup()

garch_coef_manual <- garch_coef_manual |> mutate(

gamma = 1 - alpha1 - beta1,

LR_vol = sqrt(omega / (1 - alpha1 - beta1))

)

garch_coef_manual |> select(-mu) |>

gt(rowname_col = "symbol") |>

fmt_scientific(columns = 2) |>

fmt_number(columns = 3:6, decimals = 4) | omega | alpha1 | beta1 | gamma | LR_vol | |

|---|---|---|---|---|---|

| PG | 1.06 × 10−5 | 0.1310 | 0.7744 | 0.0946 | 0.0106 |

| JPM | 9.31 × 10−6 | 0.0994 | 0.8659 | 0.0347 | 0.0164 |

| NVDA | 3.28 × 10−5 | 0.1006 | 0.8628 | 0.0366 | 0.0300 |

Plotting GARCH(1,1) volatility

# Function to calculate GARCH(1,1) variance

calculate_garch_variance <- function(returns, alpha, beta, gamma, W) {

long_run_variance <- var(returns[1:W], na.rm = TRUE)

omega <- gamma * long_run_variance

garch_var <- rep(NA, length(returns))

garch_var[W] <- var(returns[1:W]) # Initialize the first GARCH variance

for (i in (W+1):length(returns)) {

garch_var[i] <- omega + alpha * returns[i]^2 + beta * garch_var[i-1]

}

return(garch_var)

}

alpha <- 0.12; beta <- 0.78; gamma <- 1 - alpha - beta

alpha_mr <- 0.03; beta_mr <- 0.83; gamma_mr <- 1 - alpha_mr - beta_mr

# Calculate rolling GARCH(1,1) variance

all_returns_daily <- all_returns_daily |>

group_by(symbol) |>

mutate(garch_variance = calculate_garch_variance(daily.returns, alpha, beta,

gamma, W.daily),

garch_variance_mr = calculate_garch_variance(daily.returns, alpha_mr, beta_mr,

gamma_mr, W.daily)) |>

ungroup()

# Calculate the GARCH(1,1) standard deviation from the GARCH variance

all_returns_daily <- all_returns_daily |>

mutate(garch_sd = sqrt(garch_variance),

garch_sd_mr = sqrt(garch_variance_mr))

all_returns_long <- all_returns_daily |>

pivot_longer(cols = c("garch_sd", "garch_sd_mr", "ewma_sd"),

names_to = "sd_type", values_to = "sd_value")

custom_line_colors <- c("garch_sd" = color_tenor3,

"garch_sd_mr" = color_tenor2,

"ewma_sd" = color_tenor1)

custom_line_alphas <- c("garch_sd" = 1.0,

"garch_sd_mr" = 1.0,

"ewma_sd" = 0.8)

# Plot the data with ggplot2

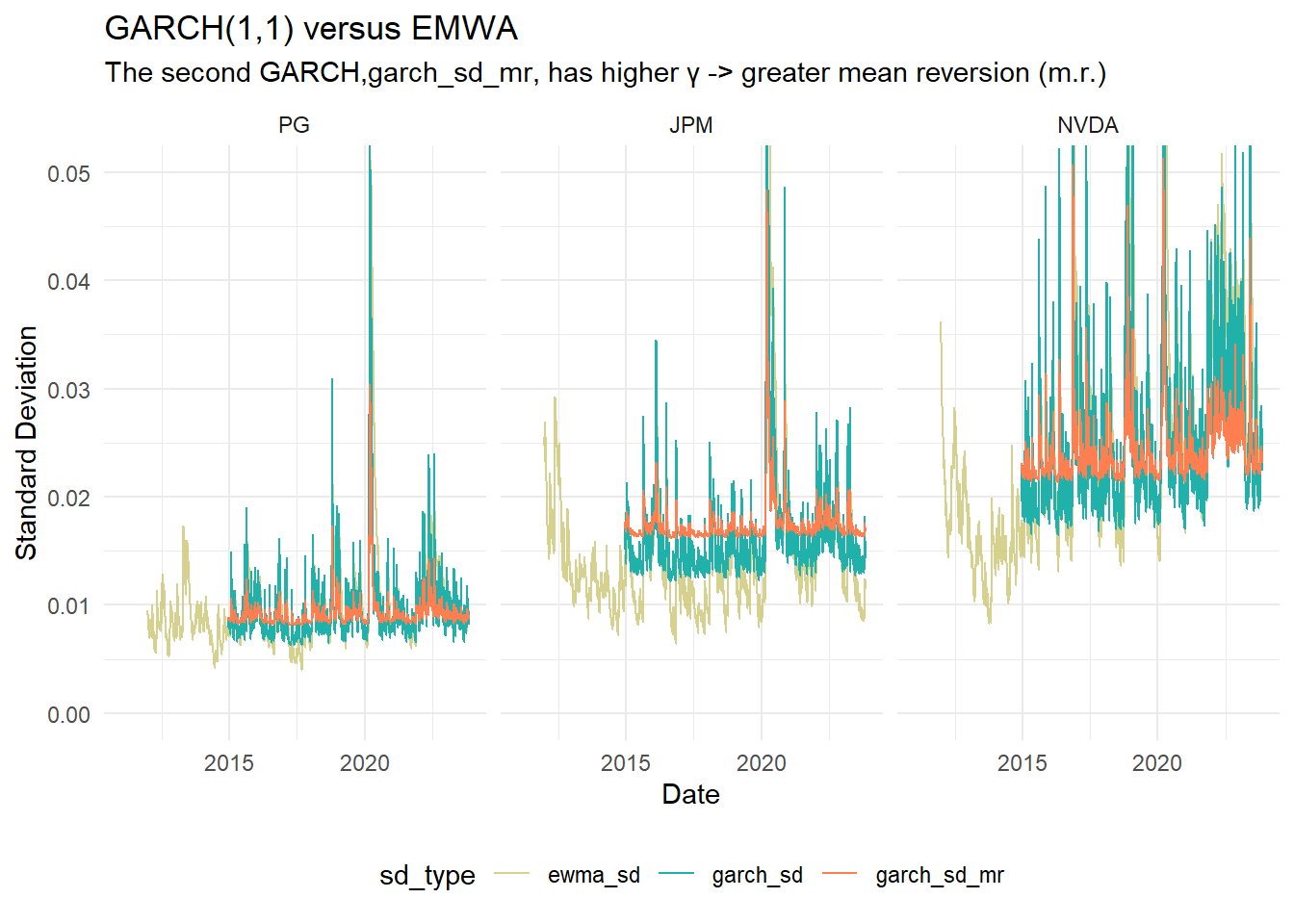

garch_p1 <- ggplot(all_returns_long, aes(x = date, y = sd_value, color = sd_type)) +

geom_line(aes(alpha = sd_type)) +

scale_color_manual(values = custom_line_colors) + # Set custom colors

scale_alpha_manual(values = custom_line_alphas) + # Set custom alphas

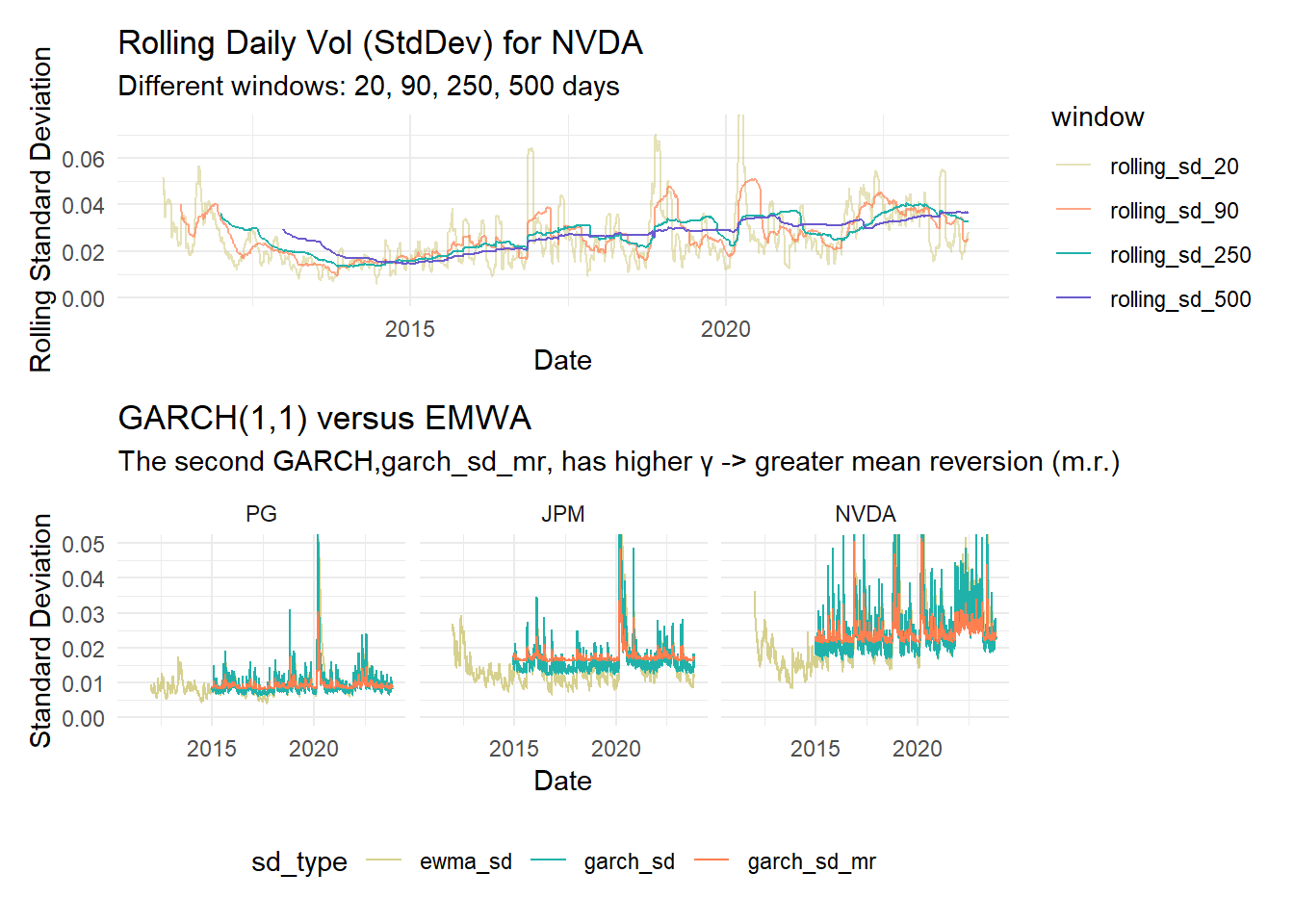

labs(title = "GARCH(1,1) versus EMWA",

subtitle = "The second GARCH,garch_sd_mr, has higher γ -> greater mean reversion (m.r.)",

x = "Date",

y = "Standard Deviation") +

facet_wrap(~symbol) +

coord_cartesian(ylim = c(0, 0.05)) +

theme_minimal() +

theme(legend.position = "bottom")

garch_p1

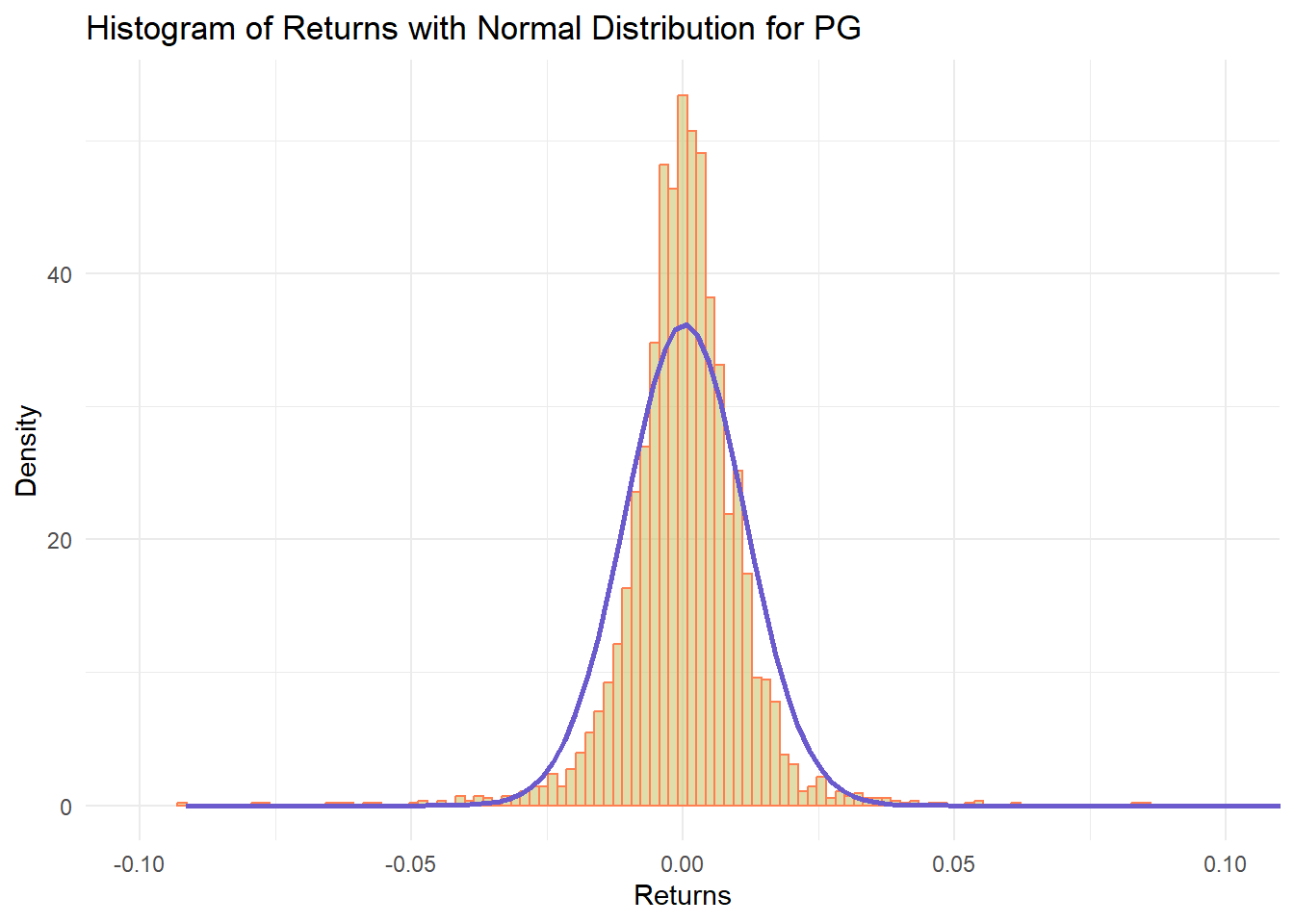

None of the returns are nearly normal

plot_histogram_with_normal <- function(stock_data, symbol, return_col) {

# Calculate mean and standard deviation of returns

mean_return <- mean(stock_data[[return_col]], na.rm = TRUE)

sd_return <- sd(stock_data[[return_col]], na.rm = TRUE)

binwidth <- (max(stock_data[[return_col]], na.rm = TRUE) -

min(stock_data[[return_col]], na.rm = TRUE)) / 120

# print(binwidth) experimenting with binwidth

# Create the histogram and overlay the normal distribution

ggplot(stock_data, aes_string(x = return_col)) +

geom_histogram(aes(y = ..density..), binwidth = binwidth,

color = "coral", fill = "khaki3", alpha = 0.6) +

stat_function(fun = dnorm, args = list(mean = mean_return, sd = sd_return),

color = "slateblue", size = 1) +

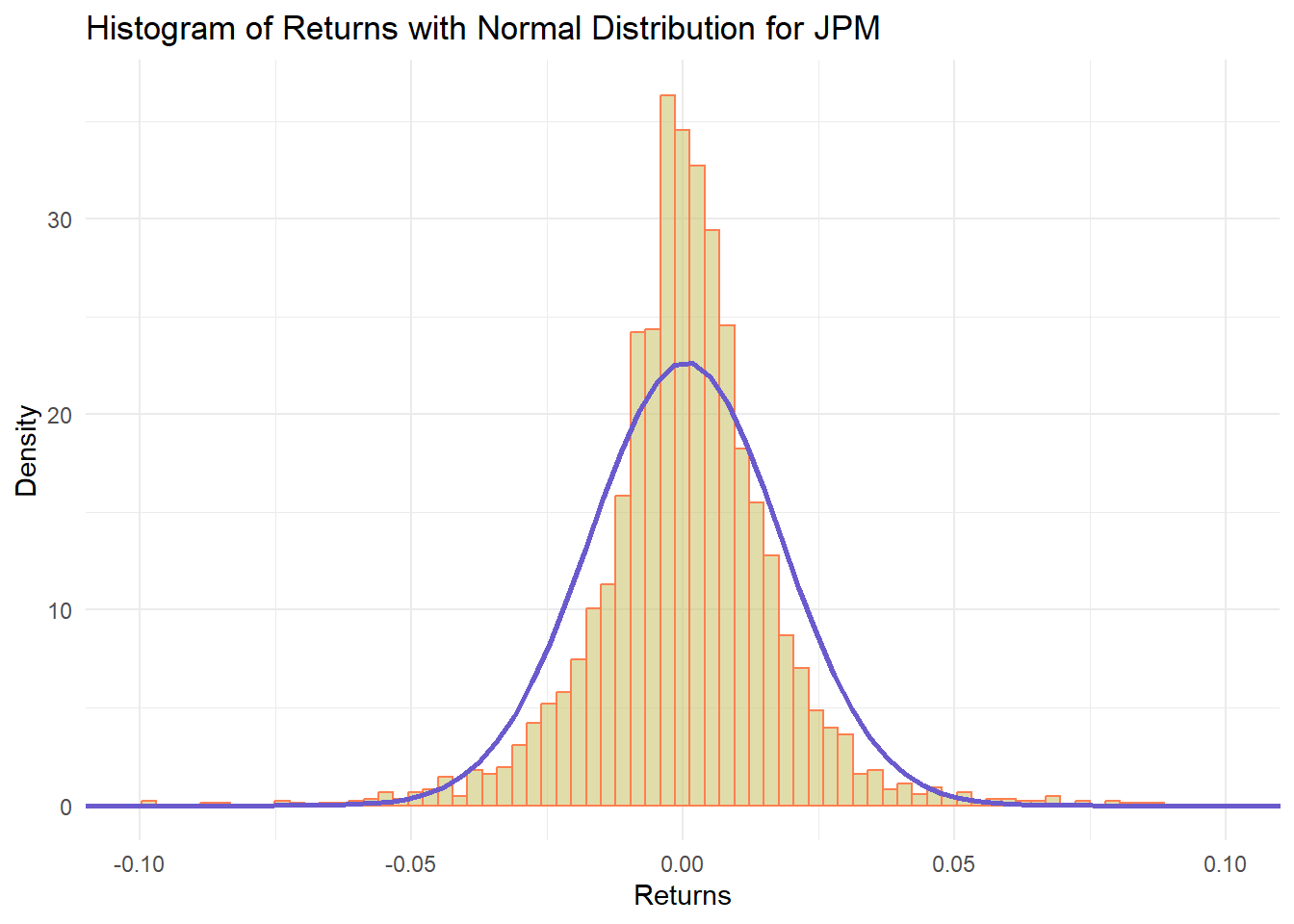

labs(title = paste("Histogram of Returns with Normal Distribution for", symbol),

x = "Returns",

y = "Density") +

theme_minimal() +

coord_cartesian(xlim = c(-0.1, 0.1))

}

jpm_hist_plot <- plot_histogram_with_normal(jpm_data, "JPM", "daily.returns")

pg_hist_plot <- plot_histogram_with_normal(pg_data, "PG", "daily.returns")

nvda_hist_plot <- plot_histogram_with_normal(nvda_data, "NVDA", "daily.returns")

jpm_hist_plot

pg_hist_plot

nvda_hist_plot

Summarize the moments

# Function to calculate the summary statistics

calculate_stats <- function(data, return_col) {

data |>

summarize(

mean = mean({{ return_col }}, na.rm = TRUE),

sd = sd({{ return_col }}, na.rm = TRUE),

skew = skewness({{ return_col }}, na.rm = TRUE),

kurt = kurtosis({{ return_col }}, na.rm = TRUE)

)

}

# Calculate statistics for each stock and store them in a tibble

stats_tibble <- tibble(

stock = c("PG", "JPM", "NVDA"),

stats = list(

calculate_stats(pg_data, daily.returns),

calculate_stats(jpm_data, daily.returns),

calculate_stats(nvda_data, daily.returns)

)

)

# Unnest the stats column to expand the tibble

stats_tibble <- stats_tibble |>

unnest(stats)

stats_tibble |> gt() |>

fmt_percent(columns = vars(mean, sd), decimals = 4) |>

fmt_number(columns = vars(skew, kurt), decimals = 4) |>

data_color(

columns = 4,

domain = c(-0.2, 0.4),

palette = c("lightpink", "seagreen1"),

alpha = 0.5

) |>

data_color(

columns = 5,

domain = c(0, 15),

palette = c("lightpink", "seagreen1"),

alpha = 0.5

)| stock | mean | sd | skew | kurt |

|---|---|---|---|---|

| PG | 0.0380% | 1.1017% | −0.0216 | 14.7342 |

| JPM | 0.0490% | 1.7601% | −0.0967 | 13.3437 |

| NVDA | 0.1509% | 2.8227% | 0.2871 | 10.6039 |

For fun (the social thumb)

nvda_roll_plot / garch_p1