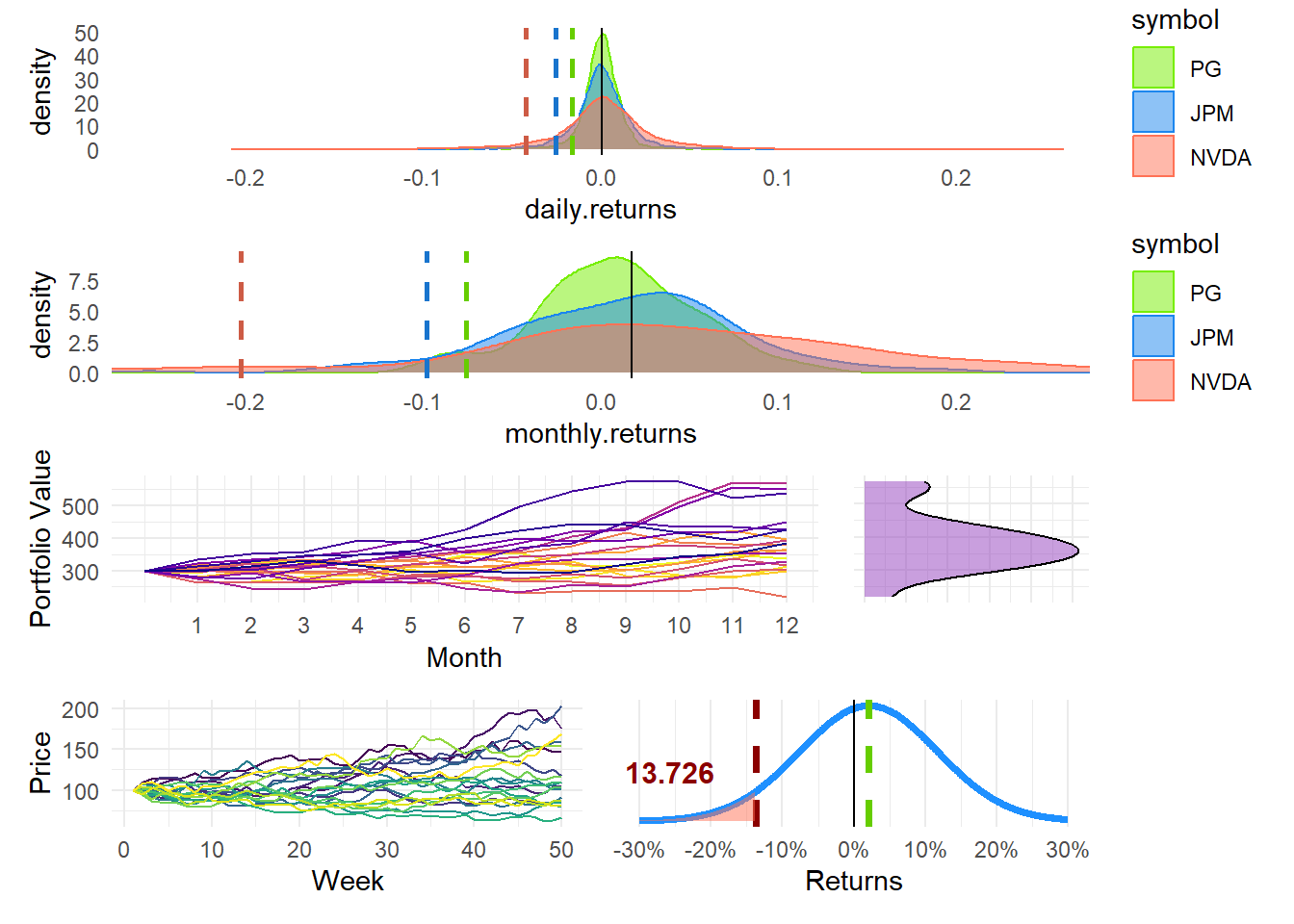

Historical simulation (basic + bootstrap, MCS, and parametric)

code

analysis

Author

David Harper, CFA, FRM

Published

November 5, 2023

Contents

Historical Simulation: Basic and Bootstrap

Monte Carlo

Parametric; aka, analytical

Historical simulation (HS)

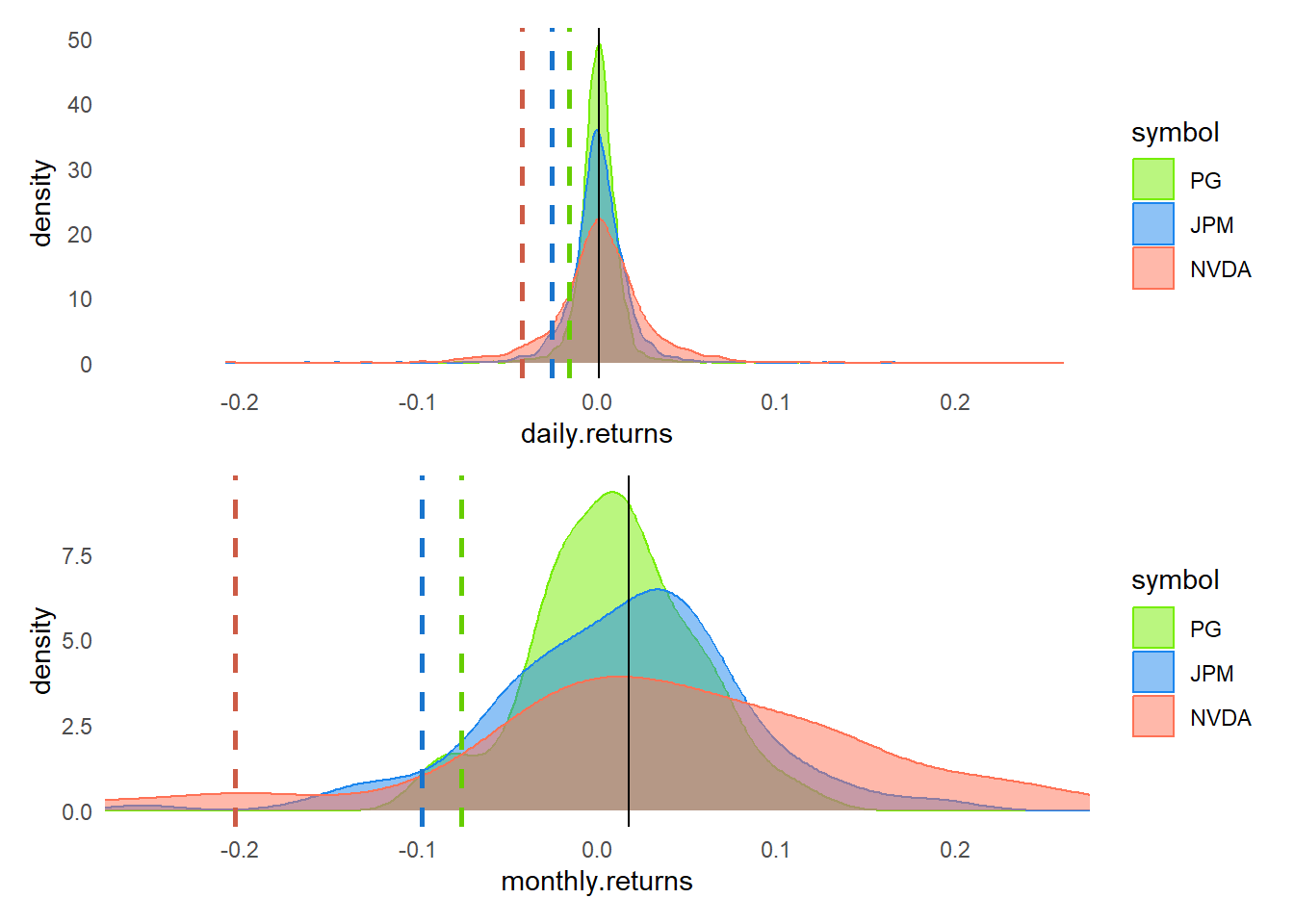

Basic HS

library(tidyverse)library(tidyquant)library(patchwork)library(scales)symbols <-c("PG", "JPM", "NVDA")mult_stocks <-tq_get(symbols, get ="stock.prices", from ="2012-12-31", to ="2022-12-31")mult_stocks$symbol <- mult_stocks$symbol <-factor(mult_stocks$symbol, levels =c("PG", "JPM", "NVDA"))# tq_mutate_fun_options() returns list of compatible mutate functions by pkg all_returns_daily <- mult_stocks |>group_by(symbol) |>tq_transmute(select = adjusted,mutate_fun = periodReturn, period ="daily", type ="log")all_returns_monthly <- mult_stocks |>group_by(symbol) |>tq_transmute(select = adjusted, mutate_fun = periodReturn, period ="monthly",type ="log")# reframe() has apparently replaced summarize()quantiles_daily <- all_returns_daily |>group_by(symbol) |>reframe(quantiles =quantile(daily.returns, probs =c(0.05, 0.95)))quantiles_monthly <- all_returns_monthly |>group_by(symbol) |>reframe(quantiles =quantile(monthly.returns, probs =c(0.05, 0.95)))# 5% quantile for each stock, DAILYPG_05d <- quantiles_daily$quantiles[1]JPM_05d <- quantiles_daily$quantiles[3]NVDA_05d <- quantiles_daily$quantiles[5]mean_d <-mean(all_returns_daily$daily.returns) # 5% quantile for each stock, MONTHLYPG_05m <- quantiles_monthly$quantiles[1]JPM_05m <- quantiles_monthly$quantiles[3]NVDA_05m <- quantiles_monthly$quantiles[5]mean_m <-mean(all_returns_monthly$monthly.returns)# I probably spend too much time tinkering with colors# col_ticker_fills <- c("PG" = "blue", "JPM" = "yellow", "NVDA" = "red")# col_ticker_fills <- c("PG" = "#90EE90", "JPM" = "#ff6347", "NVDA" = "#8B0000")col_ticker_fills <-c("PG"="chartreuse2", "JPM"="dodgerblue2", "NVDA"="coral1")col_ticker_colors <-c("PG"="chartreuse3", "JPM"="dodgerblue3", "NVDA"="coral3")col_PG_line <-"chartreuse3"; col_JPM_line <-"dodgerblue3"; col_NVDA_line <-"coral3"p_hist_daily <- all_returns_daily |>ggplot(aes(x = daily.returns, fill = symbol, color = symbol)) +geom_density(alpha =0.50) +geom_vline(xintercept = PG_05d, color = col_PG_line, linetype ="dashed", linewidth =1) +geom_vline(xintercept = JPM_05d, color = col_JPM_line, linetype ="dashed", linewidth =1) +geom_vline(xintercept = NVDA_05d, color = col_NVDA_line, linetype ="dashed", linewidth =1) +geom_vline(xintercept = mean_d, color ="black", linewidth =0.4) +scale_fill_manual(values = col_ticker_fills) +scale_color_manual(values = col_ticker_fills) +theme_minimal() +coord_cartesian(xlim =c(-0.25, 0.25)) +theme(panel.grid.major =element_blank(),panel.grid.minor =element_blank(), )p_hist_monthly <- all_returns_monthly |>ggplot(aes(x = monthly.returns, fill = symbol, color = symbol)) +geom_density(alpha =0.50) +geom_vline(xintercept = PG_05m, color = col_PG_line, linetype ="dashed", linewidth =1) +geom_vline(xintercept = JPM_05m, color = col_JPM_line, linetype ="dashed", linewidth =1) +geom_vline(xintercept = NVDA_05m, color = col_NVDA_line, linetype ="dashed", linewidth =1) +geom_vline(xintercept = mean_m, color ="black", linewidth =0.4) +scale_fill_manual(values = col_ticker_fills) +scale_color_manual(values = col_ticker_fills) +theme_minimal() +coord_cartesian(xlim =c(-0.25, 0.25)) +theme(panel.grid.major =element_blank(),panel.grid.minor =element_blank(), )p_hs <- p_hist_daily / p_hist_monthlyp_hs

Bootstrap HS

First let’s simulate a single one-year forward (+ 12 months) path

# all_returns_monthly is tidy, but the simulation wants a wide formatall_returns_monthly_wide <- all_returns_monthly |>pivot_wider(names_from = symbol, values_from = monthly.returns)# Initial investment (into each stock)initial_investment <-100portfolio <-setNames(data.frame(t(rep(initial_investment, times =length(symbols)))), symbols)months_to_simulate <-12# Set X months for the simulation# Simulate one forward monthsimulate_one_month <-function(portfolio, historical_returns_wide) {# Randomly sample one month's returns (with replacement) sampled_returns <- historical_returns_wide |>sample_n(1, replace =TRUE) |>select(-date) # Apply the sampled log returns to the current portfolio value updated_portfolio <- portfolio *exp(sampled_returns)# FOR TESTING: print(sampled_returns[1,]); print(updated_portfolio[1,])return(updated_portfolio)}# Run the simulation for X monthsset.seed(123) # For reproducibility of resultssimulation_results <-tibble(Month =0, TotalValue =sum(portfolio))for (i in1:months_to_simulate) { portfolio <-simulate_one_month(portfolio, all_returns_monthly_wide) simulation_results <- simulation_results |>add_row(Month = i, TotalValue =sum(portfolio))}print(simulation_results)

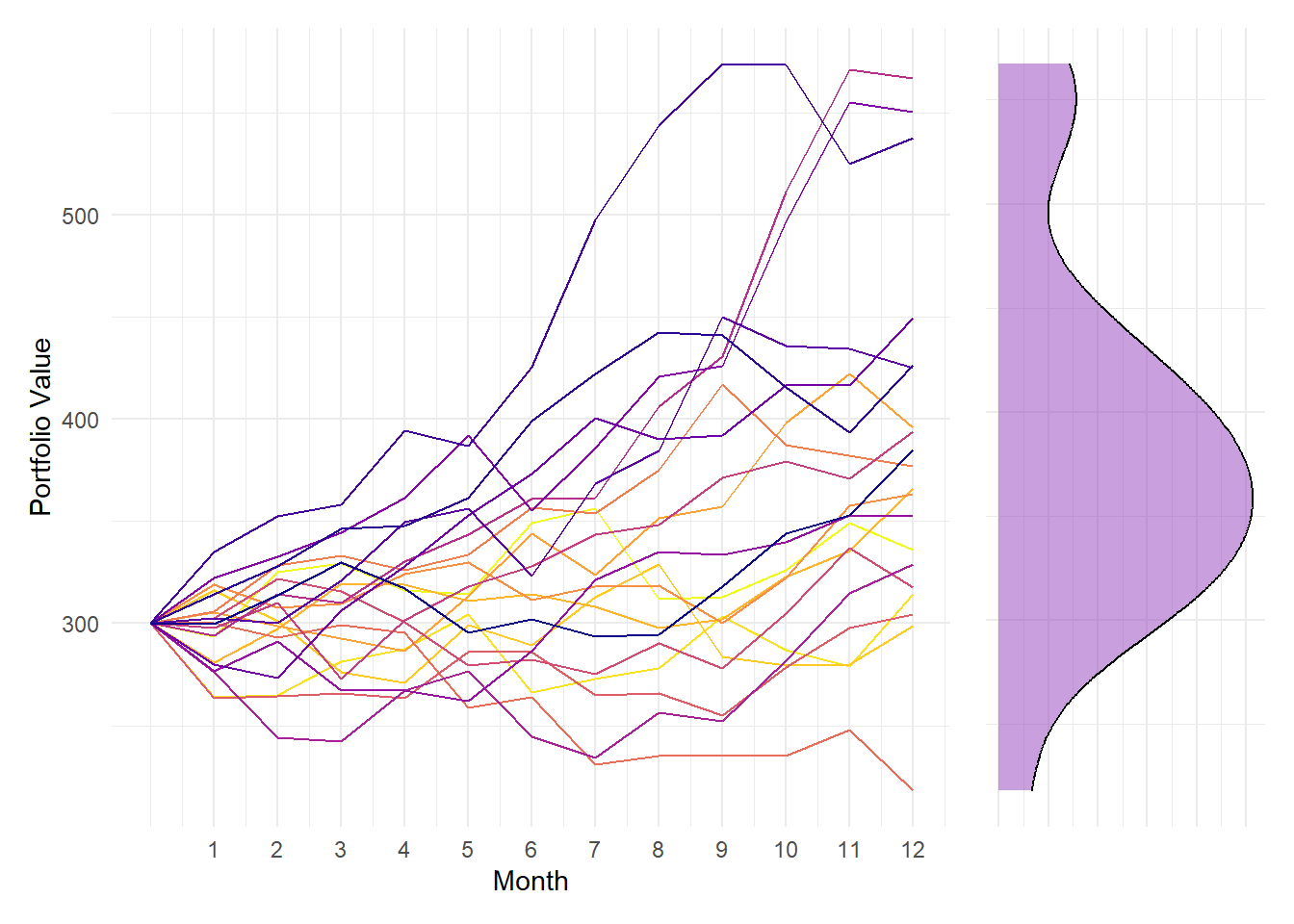

Next let’s add a loop to run the simulation multiple times; e.g. 20 trials

library(RColorBrewer)# library(ggside) couldn't pull it off! # Function to simulate portfolio over X months, where each trail has a trial_idsimulate_portfolio <-function(months_to_simulate, historical_returns_wide, initial_investment, trial_id) {# Initialize portfolio portfolio <-setNames(data.frame(t(rep(initial_investment, times =length(symbols)))), symbols)# Initialize results data frame with Month 0 simulation_results <-tibble(Month =0, TotalValue =sum(portfolio), Trial =as.factor(trial_id))for (i in1:months_to_simulate) { portfolio <-simulate_one_month(portfolio, historical_returns_wide) simulation_results <- simulation_results |>add_row(Month = i, TotalValue =sum(portfolio), Trial =as.factor(trial_id)) }return(simulation_results)}months_to_simulate <-12num_trials <-20# Number of trialsset.seed(123) all_trials <-map_df(1:num_trials, ~simulate_portfolio(months_to_simulate, all_returns_monthly_wide, initial_investment, .x), .id ="Trial_ID")final_month_values_df <- all_trials |>filter(Month ==max(all_trials$Month))# Plot the results using ggplot2p_forward_sim <-ggplot(all_trials, aes(x = Month, y = TotalValue, group = Trial, color = Trial)) +geom_line() +scale_color_viridis_d(option ="plasma", direction =-1) +theme_minimal() +scale_x_continuous(breaks =1:12, limits =c(0,12)) +labs(x ="Month",y ="Portfolio Value") +theme(legend.position ="none") density_plot <- final_month_values_df |>ggplot(aes(x = TotalValue)) +geom_density(fill ="#933fbd", alpha =0.5) +theme_minimal() +theme(axis.title =element_blank(),axis.text =element_blank() ) +coord_flip()p_boot <- p_forward_sim + density_plot +plot_layout(ncol =2, widths =c(3, 1))p_boot

final_month_values_vct <- final_month_values_df |>pull(TotalValue) # 'pull' extracts the column as a vector# Calculate and print the quantiles for the final month's valuesquantiles_final_month <-quantile(final_month_values_vct, probs =c(0, 0.01, 0.05, 0.50, 1.0))print(quantiles_final_month)