library(tidyverse); library(gt)

library(patchwork)

library(broom); library(performance); library(lmtest)

library(desk)Contents

- Illustration of residual sum of squares (RSS) with n = 12 subset

- Univariate (aka, simple) linear regression: AAPL vs S&P 1500, n = 72 months

- Model diagnostics

- Autocorrelation test

Loading packages

Regressing Apple’s (AAPL) returns against S&P 1500

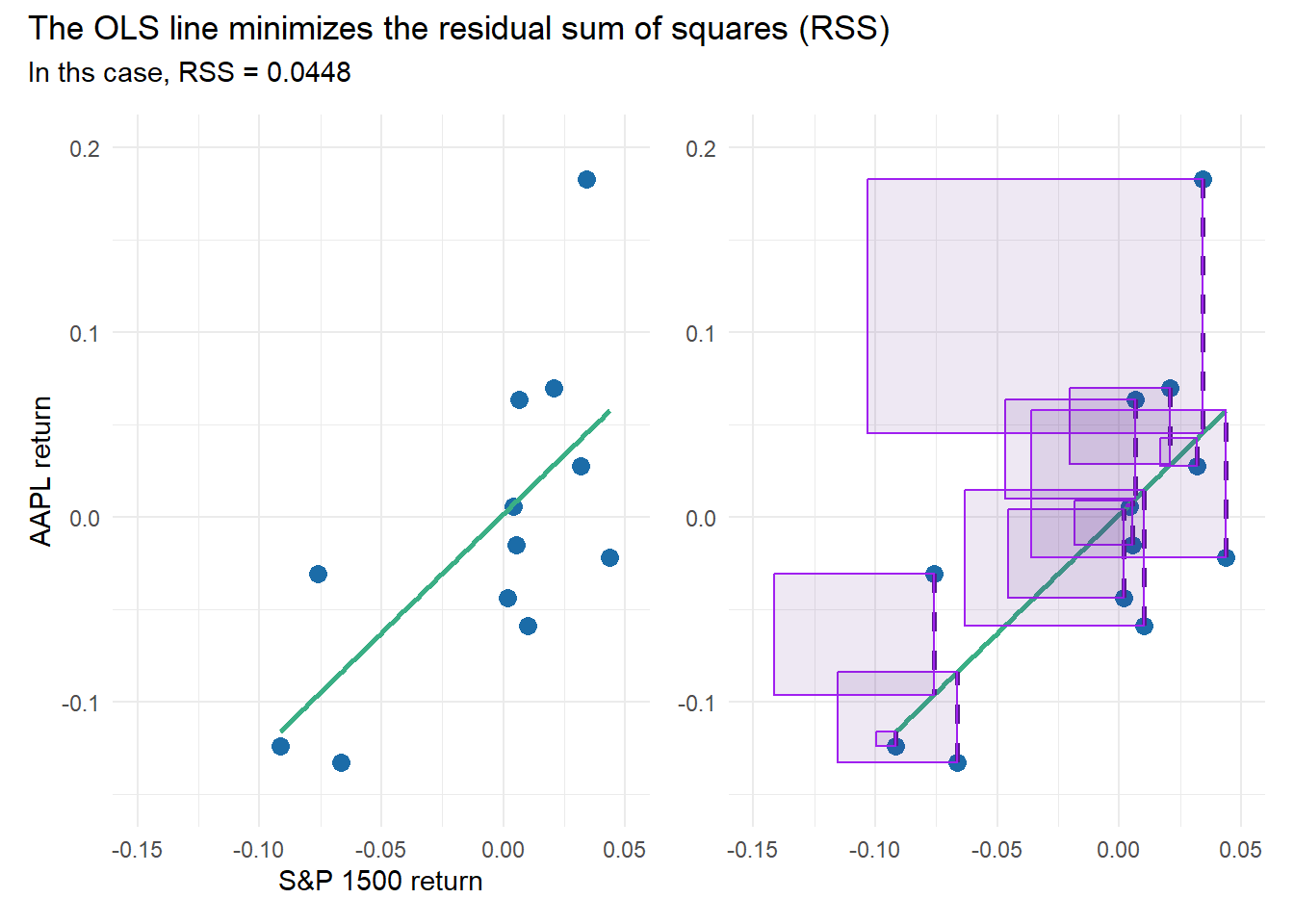

Subset of 12 months just to illustrate RSS boxes

The full set is 72 months of returns. The sample of 12 months is just to illustrate the residual sum of squares (RSS) concept; the squares are less cluttered.

data_72 <- readRDS("t2-20-17-aapl-sp1500.rds") # 72 monthly returns

row.names(data_72) <- 1:nrow(data_72)

model_72 <- lm(r_m_AAPL ~ r_SP_1500, data = data_72) # linear model

set.seed(97531) # Adding Y ~ X just because they're familiar axes

data_12 <- sample_n(data_72, 12) # sample of 12 monthly returns

data_12$y <- data_12$r_m_AAPL # just to illustrate RSS

data_12$x <- data_12$r_SP_1500

model_12 <- lm(y ~ x, data=data_12) # linear model

data_12$residuals <- residuals(model_12)

sum(model_12$residuals^2)[1] 0.0448225RSS <- sum(model_12$residuals^2)

pred_Y <- predict(model_12)

cooks_d <- cooks.distance(model_12)

# colors for plots

green_line = "#3aaf85"; blue_points = "#1b6ca8"; red_color = "#cd201f"

p0 <- data_12 |> ggplot(aes(x=x, y=y)) +

geom_point(size=3, color=blue_points) +

geom_smooth(method="lm", se=FALSE, color=green_line)

p1 <- p0 +

theme_minimal() +

xlab("S&P 1500 return") +

ylab("AAPL return") +

coord_cartesian(xlim = c(-0.15, 0.05), ylim = c(-0.15, 0.20))

p2 <- p0 +

geom_segment(aes(xend=x, yend=y - residuals), color="purple4", linewidth = 1, linetype = "dashed") +

geom_rect(aes(xmin = x - abs(residuals),

xmax = x,

ymin = ifelse(residuals > 0, y - abs(residuals), y),

ymax = ifelse(residuals > 0, y, y + abs(residuals))),

fill="purple4", color="purple", linewidth=0.5, alpha = 0.10) +

theme_minimal() +

theme(axis.title = element_blank()) +

coord_cartesian(xlim = c(-0.15, 0.05), ylim = c(-0.15, 0.20))

scatter_pw <- p1 + p2

scatter_pw + plot_annotation(

title = "The OLS line minimizes the residual sum of squares (RSS)",

subtitle = sprintf("In ths case, RSS = %.4f", RSS)

)

# To show the residuals in a gt table

result_df <- data.frame(

X = data_12$x,

Y = data_12$y,

Pred_Y = pred_Y,

residual = model_12$residuals,

residual_sq = model_12$residuals^2,

cooksD = cooks_d

)

# But sorting by X = SP1500

result_df_sorted <- result_df[order(result_df$X), ]

result_df_sorted_tbl <- gt(result_df_sorted)

p1_tbl <- result_df_sorted_tbl |>

fmt_percent(

columns = 1:4,

decimals = 2

) |>

fmt_number(

columns = 5:6,

decimals = 5

) |>

cols_label(

X = md("**S&P 1500**"),

Y = md("**AAPL**"),

Pred_Y = md("**Pred(AAPL)**"),

residual = md("**Residual**"),

residual_sq = md("**Residual^2**"),

cooksD = md("**Cook's D**")

) |>

data_color(

columns = 5,

palette = c("white","purple4"),

domain = c(0,0.02),

na_color = "lightgrey"

) |>

data_color(

columns = 6,

palette = c("white","purple4"),

domain = c(0,0.50),

na_color = "lightgrey"

) |>

tab_options(

table.font.size = 12

)

p1_tbl| S&P 1500 | AAPL | Pred(AAPL) | Residual | Residual^2 | Cook’s D |

|---|---|---|---|---|---|

| −9.15% | −12.41% | −11.61% | −0.80% | 0.00006 | 0.00797 |

| −7.60% | −3.10% | −9.62% | 6.53% | 0.00426 | 0.28504 |

| −6.64% | −13.26% | −8.38% | −4.88% | 0.00238 | 0.11176 |

| 0.19% | −4.36% | 0.40% | −4.76% | 0.00226 | 0.02610 |

| 0.42% | 0.58% | 0.70% | −0.12% | 0.00000 | 0.00002 |

| 0.55% | −1.51% | 0.86% | −2.37% | 0.00056 | 0.00675 |

| 0.66% | 6.34% | 1.00% | 5.34% | 0.00285 | 0.03485 |

| 1.00% | −5.89% | 1.44% | −7.34% | 0.00538 | 0.06959 |

| 2.09% | 6.95% | 2.84% | 4.11% | 0.00169 | 0.02787 |

| 3.18% | 2.76% | 4.25% | −1.49% | 0.00022 | 0.00499 |

| 3.42% | 18.27% | 4.55% | 13.72% | 0.01883 | 0.45582 |

| 4.37% | −2.18% | 5.77% | −7.95% | 0.00632 | 0.20839 |

Let’s see the effect of removing the most influential observation:

influential_obs <- which.max(cooks_d)

data_11_no_influential <- data_12[-influential_obs, ]

model_11_no_influential <- lm(y ~ x, data = data_11_no_influential)

coef_original <- coef(model_12)

coef_no_influential <- coef(model_11_no_influential)

comparison <- data.frame(Original = coef_original, Minus_Influential = coef_no_influential)

comparison Original Minus_Influential

(Intercept) 0.001526393 -0.01380419

x 1.285736582 0.99796665equation_label_p1 <- sprintf("Y = %.3f + %.3fX", coef_original[1], coef_original[2])

equation_label_p1i <- sprintf("Y = %.3f + %.3fX", coef_no_influential[1], coef_no_influential[2])

p1 <- p1 +

geom_vline(xintercept = 0, linetype = "dashed", color = "black") + # X = 0 axis

geom_hline(yintercept = 0, linetype = "dashed", color = "black") + # Y = 0 axis

annotate("text", x = -0.08, y = 0.15, label = equation_label_p1,

size = 5.0, color = "black")

p1i <- data_11_no_influential |> ggplot(aes(x=x, y=y)) +

geom_point(size=3, color=blue_points) +

geom_smooth(method="lm", se=FALSE, color=green_line) + # Adding regression line

geom_vline(xintercept = 0, linetype = "dashed", color = "black") + # X = 0 axis

geom_hline(yintercept = 0, linetype = "dashed", color = "black") + # Y = 0 axis

annotate("text", x = -0.08, y = 0.15, label = equation_label_p1i,

size = 5.0, color = "black") +

theme_minimal() +

theme(axis.title = element_blank()) +

coord_cartesian(xlim = c(-0.15, 0.05), ylim = c(-0.15, 0.20))

p1 + p1i

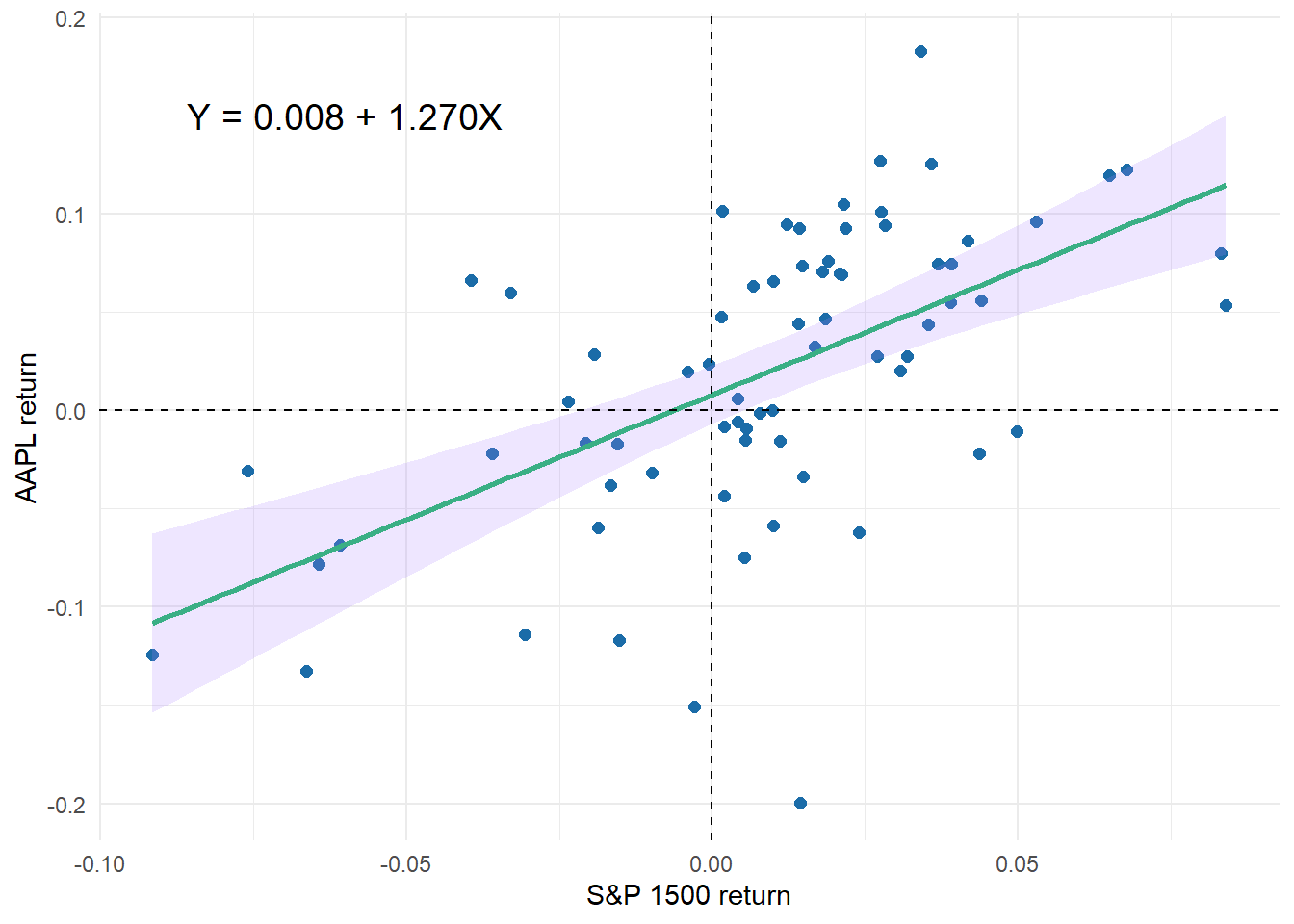

The full dataset of 72 monthly returns

row.names(data_72) <- 1:nrow(data_72)

model_72 <- lm(r_m_AAPL ~ r_SP_1500, data = data_72)

model_72_coeff <- coef(model_72)

equation_label_72 <- sprintf("Y = %.3f + %.3fX", model_72_coeff[1], model_72_coeff[2])

p1_model_72 <- data_72 %>% ggplot(aes(r_SP_1500, r_m_AAPL)) +

geom_point(size = 2, color = blue_points) +

geom_smooth(method = "lm", color = green_line, fill = "mediumpurple1", alpha = 0.20) +

geom_vline(xintercept = 0, linetype = "dashed", color = "black") + # X = 0 axis

geom_hline(yintercept = 0, linetype = "dashed", color = "black") + # Y = 0 axis

theme_minimal() +

xlab("S&P 1500 return") +

ylab("AAPL return") +

annotate("text", x = -0.06, y = 0.15, label = equation_label_72,

size = 5.0, color = "black")

p1_model_72

summary(model_72) # Just to show the standard/typical output

Call:

lm(formula = r_m_AAPL ~ r_SP_1500, data = data_72)

Residuals:

Min 1Q Median 3Q Max

-0.226290 -0.027060 0.002344 0.040667 0.131313

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.007969 0.007477 1.066 0.29

r_SP_1500 1.269625 0.215600 5.889 1.23e-07 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.06123 on 70 degrees of freedom

Multiple R-squared: 0.3313, Adjusted R-squared: 0.3217

F-statistic: 34.68 on 1 and 70 DF, p-value: 1.23e-07Model output in gt table

model_72_tidy <- tidy(model_72)

gt_table_model_72 <- gt(model_72_tidy)

gt_table_model_72 <-

gt_table_model_72 %>%

tab_options(

table.font.size = 14

) %>%

tab_style(

style = cell_text(weight = "bold"),

locations = cells_body()

) %>%

tab_header(

title = "AAPL versus S&P_1500: Gross (incl. Rf) monthly log return",

subtitle = md("Six years (2014 - 2019), n = 72 months")

) %>%

tab_source_note(

source_note = "Source: tidyquant https://cran.r-project.org/web/packages/tidyquant/"

) %>% cols_label(

term = "Coefficient",

estimate = "Estimate",

std.error = "Std Error",

statistic = "t-stat",

p.value = "p value"

) %>% fmt_number(

columns = vars(estimate, std.error, statistic),

decimals = 3

) %>% fmt_scientific(

columns = vars(p.value),

) %>%

tab_options(

heading.title.font.size = 14,

heading.subtitle.font.size = 12

)

gt_table_model_72| AAPL versus S&P_1500: Gross (incl. Rf) monthly log return | ||||

|---|---|---|---|---|

| Six years (2014 - 2019), n = 72 months | ||||

| Coefficient | Estimate | Std Error | t-stat | p value |

| (Intercept) | 0.008 | 0.007 | 1.066 | 2.90 × 10−1 |

| r_SP_1500 | 1.270 | 0.216 | 5.889 | 1.23 × 10−7 |

| Source: tidyquant https://cran.r-project.org/web/packages/tidyquant/ | ||||

The table above is featured in one of my practice questions:

Answer: C. True: 90.0% CI = (0.91; 1.63)

The two-tailed critical-Z at 90.0% confidence is 1.645 such that the CI = 1.270 +/- 1.645 × 0.216 = (0.91; 1.63). The confidence interval is given by: coefficient ± (standard error) × (critical value). The sample size is large so we can use the normal deviate of 1.645 associated with 90.0% two-tailed confidence; note this should not require any lookup because we already know the 95.0% confident one-tailed normal deviate is 1.645. With 70 degrees of freedom, the critical t value is T.INV.2T(0.10, 70) = 1.666914, so we can see that normal Z is a close approximation.

# Confidence interval around the slope

beta <- model_72_tidy$estimate[2]

se_beta <- model_72_tidy$std.error[2]

ci_confidence = 0.90

z_2s <- qnorm((1 + ci_confidence)/2)

ci_lower <- beta - se_beta*z_2s

ci_upper <- beta + se_beta*z_2s

ci_lower[1] 0.9149948ci_upper[1] 1.624256Model diagnostics

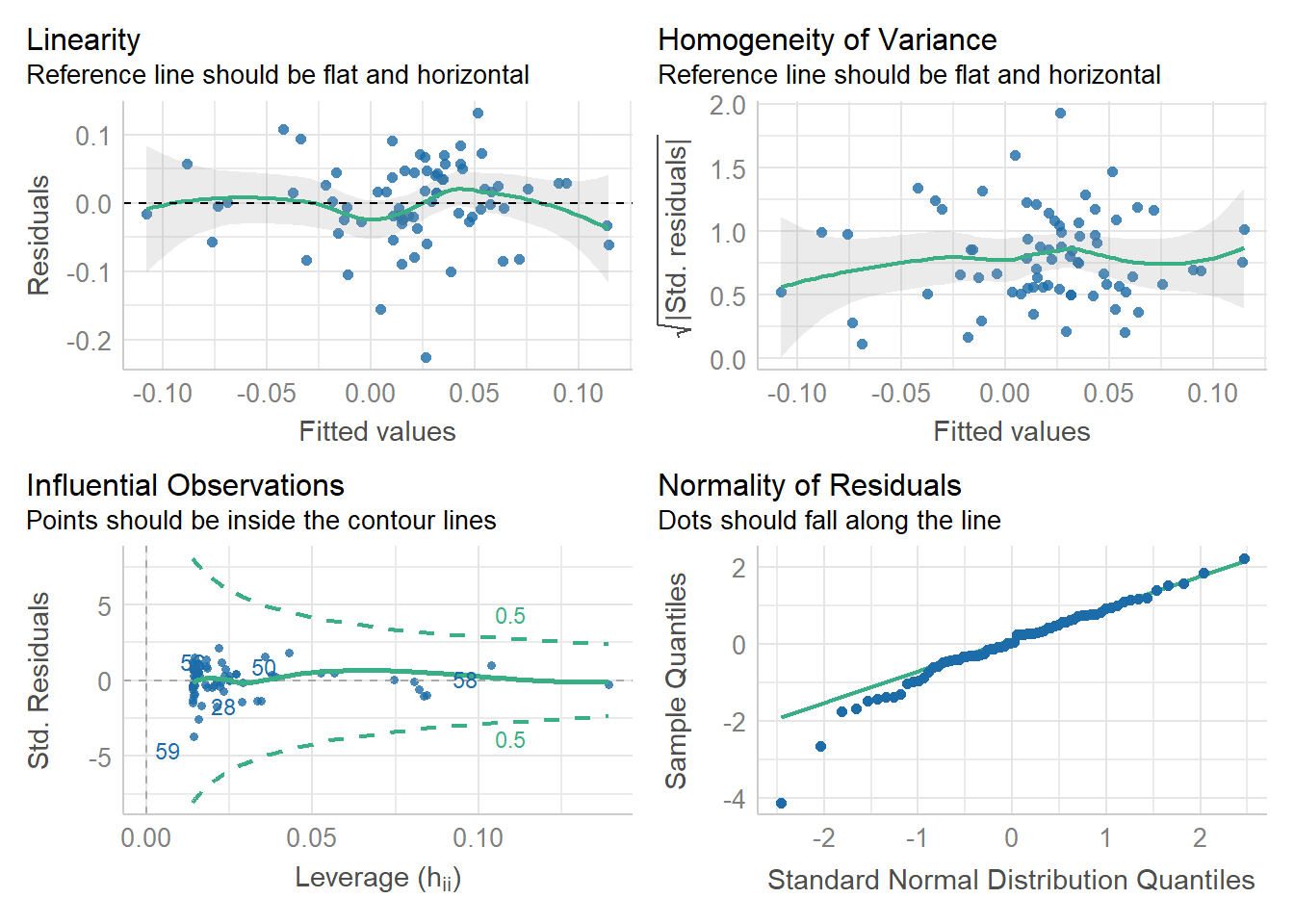

There are many choices but I like the performance package.

check_model(model_72, check = c("linearity", "homogeneity", "outliers", "qq"))

In regard to the above:

- Linearity plot; aka, Tukey-Anscombe

- Homogeneity (of variance); aka, scale-location plot

- Outliers (Influential Observations) uses Cook’s distance

- Q-Q plot is test of residual normality

Both of the first two plots (upper row) can be used to check for heteroscedasticity. The second is supposedly better: by rooting the absolute value, differences are amplified. Notice it’s Y-axis (Homogeneity of Variance) is non-negative such that the “perfect” reference line is nearer to one than zero.

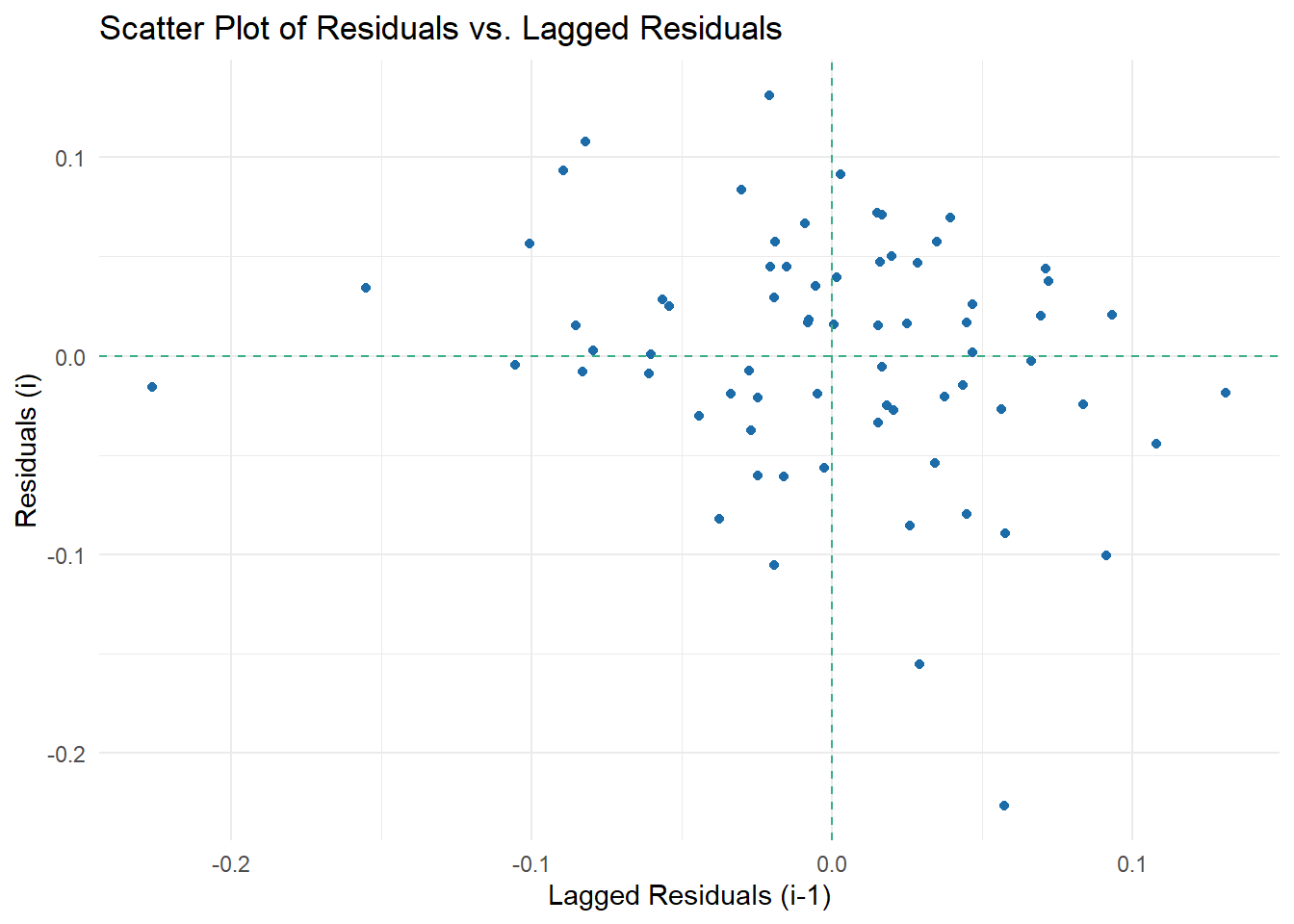

Autocorrelation tests

First, Durbin-Watson with check_autocorrelation() in performance package:

check_autocorrelation(model_72)OK: Residuals appear to be independent and not autocorrelated (p = 0.068).Let’s plot residual against lag 1 residual.

residuals_72 <- residuals(model_72)

lagged_residuals_72 <- c(NA, residuals_72[-length(residuals_72)])

residual_data <- data.frame(

Residuals = residuals_72[-1], # Exclude the first value as it doesn't have a lagged residual

Lagged_Residuals = lagged_residuals_72[-1] # Exclude the last value as it is NA

)

ggplot(residual_data, aes(x = Lagged_Residuals, y = Residuals)) +

geom_point(color = blue_points) +

labs(title = "Scatter Plot of Residuals vs. Lagged Residuals",

x = "Lagged Residuals (i-1)",

y = "Residuals (i)") +

geom_hline(yintercept = 0, linetype = "dashed", color = green_line) +

geom_vline(xintercept = 0, linetype = "dashed", color = green_line) +

theme_minimal()

linear_model <- lm(Residuals ~ Lagged_Residuals, data = residual_data)

linear_model

Call:

lm(formula = Residuals ~ Lagged_Residuals, data = residual_data)

Coefficients:

(Intercept) Lagged_Residuals

0.001015 -0.218861 cor(residual_data$Residuals, residual_data$Lagged_Residuals)[1] -0.2207468summary(linear_model)$r.squared[1] 0.04872914cor(residual_data$Residuals, residual_data$Lagged_Residuals)^2[1] 0.04872914Finally, let’s try dw.test from the desk package which is new but looks good:

dw.test(model_72, dir = "right")

Durbin-Watson Test on AR(1) autocorrelation

--------------------------------------------

Hypotheses:

H0: H1:

d <= 2 (rho >= 0, no neg. a.c.) d > 2 (rho < 0, neg. a.c.)

Test results:

dw crit.value p.value sig.level H0

2.3979 2.3765 0.0411 0.05 rejecteddw.test(model_72, dir = "both")

Durbin-Watson Test on AR(1) autocorrelation

--------------------------------------------

Hypotheses:

H0: H1:

d = 2 (rho = 0, no a.c.) d <> 2 (rho <> 0, a.c.)

Test results:

dw crit.value p.value sig.level H0

2.3979 2.4482 0.0821 0.05 not rejected