library(tidyverse); library(patchwork); library (ggcorrplot); library(gt)

library(tidyquant)

library(MASS) # write.matrix

# library(dplyr); library(tidyr); library(purrr)

# library(ggplot)Contents

- Define the potential portfolios (= sets of assets)

- Retrieve returns for each periodicity; aka, frequency

- Add analysis list-column: volatility, avg return, correlation matrix

- Correlation

- Single stocks are better diversifiers

- Visualize correlation

- Simulation

- Select the portfolio (set)

- Bias the random weights

- Setup the simulation; i.e., functions

- Run the simulation

- Visualize

- Add a second CML

Define the potential portfolios (= sets of assets)

The container in this approach is stock_sets, a dataframe we initialize (as our TOC) with three columns:

- set_id

- description

- symbols: a list of tickers

Each row of the stock_sets dataframe hold an entire portfolio including these identifiers plus the returns (via nested_data), and the analysis. The latter two are added as list-columns which are versatile objects: list-items can include dataframes, vectors, and even other lists.

# First row of stock_sets is (portfolio of) sector ETFs:

sector_11etf_list <- c("XLK", # Technology

"XLV", # Health Care

"XLF", # Financials

"XLY", # Consumer Discretionary

"XLP", # Consumer Staples

"XLE", # Energy

"XLU", # Utilities

"XLI", # Industrials

"XLB", # Materials

"XLRE", # Real Estate

"XLC") # Communication Services

# Second row of stock_sets is (portfolio of) style ETFs:

size_style_etfs <- c("IWF", # Large-Cap Growth

"IWD", # Large-Cap Value

"SPY", # Large-Cap Blend

"IWP", # Mid-Cap Growth

"IWS", # Mid-Cap Value

"MDY", # Mid-Cap Blend

"IWO", # Small-Cap Growth

"IWN", # Small-Cap Value

"IWM") # Small-Cap Blend

# Third row is largest (by market cap) company in each sector:

large_mid_caps <- read_csv("large_mid_caps.csv")

large_mid_caps <- large_mid_caps |> rename_at('Market Cap', ~ 'Capitalization')

large_mid_caps$Industry <- as_factor(large_mid_caps$Industry)

large_mid_caps$Sector <- as_factor(large_mid_caps$Sector)

# select the largest (by Market Cap) in each Industry

top_in_sector <- large_mid_caps |>

group_by(Sector) |>

arrange(desc(Capitalization)) |>

slice(1)

remove_rows <- c(7, 8, 15, 17)

top_in_sector <- top_in_sector[-remove_rows,]

# This is the essential stock_sets dataframe

stock_sets <- tibble(

set_id = c("11_sectors",

"9_styles",

"13_top_in_sector"),

description = c("All 11 Sectors",

"All 9 Styles",

"Top Market Cap in each of 13 Sectors"),

# this is a list column, see https://adv-r.hadley.nz/vectors-chap.html#list-columns

symbols = list(sector_11etf_list, size_style_etfs, top_in_sector$Ticker)

)

date_start <- "2013-01-01"

date_end <- "2023-11-17"Retrieve returns for each frequency; aka, periodicity

Each portfolio is a set of tickers/symbols. For each of the portfolio’s symbols (aka, tickers), the get_returns function retrieves log returns into three dataframes; one for each frequency:

- daily

- weekly

- monthly

We will call the get_returns function via map (purrr is one of my favorite packagse!) to create a new list column called nested_data. Each row of nested_data will contain a list of three dataframes, one for each period. These dataframes will contain the log returns for each ticker in the set.

# This will add the nested_data list-column. For example, we

# can use stock_sets$nested_data[[n]]$daily$daily.returns to

# retrieve daily.returns for the nth portfolio

get_returns <- function(symbols, start_date, end_date) {

mult_stocks <- tq_get(symbols, get = "stock.prices",

from = start_date, to = end_date)

periods <- c("daily", "weekly", "monthly")

returns_list <- lapply(periods, function(period) {

mult_stocks |>

group_by(symbol) |>

tq_transmute(select = adjusted,

mutate_fun = periodReturn,

period = period,

type = "log")

})

names(returns_list) <- periods

return(returns_list)

}

# Nest return data for each stock set

stock_sets <- stock_sets |>

mutate(nested_data = map(symbols,

~ get_returns(.x, date_start, date_end)))

print(stock_sets)# A tibble: 3 × 4

set_id description symbols nested_data

<chr> <chr> <list> <list>

1 11_sectors All 11 Sectors <chr [11]> <named list>

2 9_styles All 9 Styles <chr [9]> <named list>

3 13_top_in_sector Top Market Cap in each of 13 Sectors <chr [13]> <named list>Add analysis list-column: volatility, avg return, correlation matrix

For each portfolio (set of tickers) and periodicity, the analysis list column generates:

- vector of volatilities

- vector of average returns

- correlation matrix (diagonal is 1)

- average correlation (as a rough measure of diversification)

# For example, we can use stock_sets$analysis[[1]]$monthly$corr_matrix

# to retrieve the correlation matrix for the nth portfolio

perform_analysis <- function(data, frequency) {

# Determine the column name for returns based on the frequency

returns_col <- switch(frequency,

"daily" = "daily.returns",

"weekly" = "weekly.returns",

"monthly" = "monthly.returns",

stop("Invalid frequency"))

# Calculate volatilities

volatilities <- data |>

group_by(symbol) |>

summarise(volatility = sd(.data[[returns_col]], na.rm = TRUE)) |>

ungroup()

# Calculate average returns

avg_returns <- data |>

group_by(symbol) |>

summarise(avg_return = mean(.data[[returns_col]], na.rm = TRUE)) |>

ungroup()

# Pivot to wide format for correlation matrix calculation

data_wide <- data |>

group_by(date) |>

pivot_wider(names_from = symbol, values_from = .data[[returns_col]])

# Write files to verify (in Excel) the correlation matrix

# write.csv(data_wide, paste0("data_wide_", frequency, ".csv"), row.names = FALSE)

# Calculate the correlation matrix

corr_matrix <- cor(data_wide[ ,-1], use = "complete.obs")

# write.csv(as.data.frame(corr_matrix), paste0("corr_matrix_", frequency, ".csv"), row.names = TRUE)

# Calculate average correlation

avg_corr <- mean(corr_matrix[lower.tri(corr_matrix)])

return(list(volatilities = volatilities,

avg_returns = avg_returns,

corr_matrix = corr_matrix,

avg_corr = avg_corr))

}

# Applying the perform_analysis function to the stock_sets

stock_sets <- stock_sets |>

mutate(analysis = map(nested_data, ~ {

list(

daily = perform_analysis(.x$daily, "daily"),

weekly = perform_analysis(.x$weekly, "weekly"),

monthly = perform_analysis(.x$monthly, "monthly")

)

}))

# Examine data structure

print(stock_sets)# A tibble: 3 × 5

set_id description symbols nested_data analysis

<chr> <chr> <list> <list> <list>

1 11_sectors All 11 Sectors <chr> <named list> <named list>

2 9_styles All 9 Styles <chr> <named list> <named list>

3 13_top_in_sector Top Market Cap in each of … <chr> <named list> <named list>glimpse(stock_sets)Rows: 3

Columns: 5

$ set_id <chr> "11_sectors", "9_styles", "13_top_in_sector"

$ description <chr> "All 11 Sectors", "All 9 Styles", "Top Market Cap in each …

$ symbols <list> <"XLK", "XLV", "XLF", "XLY", "XLP", "XLE", "XLU", "XLI", "…

$ nested_data <list> [[<grouped_df[28057 x 3]>], [<grouped_df[5819 x 3]>], [<g…

$ analysis <list> [[[<tbl_df[11 x 2]>], [<tbl_df[11 x 2]>], <<matrix[11 x 1…Correlation

Average average correlation

# GPT4 basically wrote this entire chunk: I added it while writing substack

# Prepare a dataframe for the average correlations

avg_corr_data <- tibble(

Portfolio = character(),

Frequency = character(),

Average_Correlation = numeric()

)

# Loop through each portfolio and each frequency

for (i in seq_along(stock_sets$analysis)) {

portfolio_id <- stock_sets$set_id[i]

for (freq in c("daily", "weekly", "monthly")) {

avg_corr <- stock_sets$analysis[[i]][[freq]]$avg_corr

avg_corr_data <- avg_corr_data |>

add_row(

Portfolio = portfolio_id,

Frequency = freq,

Average_Correlation = avg_corr

)

}

}

# Create a wider table format

avg_corr_wide <- avg_corr_data |>

pivot_wider(

names_from = Frequency,

values_from = Average_Correlation,

names_prefix = "Avg_Corr_"

)

# Add a column for the overall average correlation

avg_corr_wide <- avg_corr_wide |>

rowwise() |>

mutate(Avg_Corr_Total = mean(c_across(starts_with("Avg_Corr_")), na.rm = TRUE)) |>

ungroup()

avg_corr_wide |>

gt() |>

tab_header(title = "Average Correlation per Frequency") |>

cols_label(

Portfolio = "Portfolio",

Avg_Corr_daily = "Daily",

Avg_Corr_weekly = "Weekly",

Avg_Corr_monthly = "Monthly",

Avg_Corr_Total = "Avg Avg Corr"

) |>

fmt_number(columns = 2:5, decimals = 3)| Average Correlation per Frequency | ||||

|---|---|---|---|---|

| Portfolio | Daily | Weekly | Monthly | Avg Avg Corr |

| 11_sectors | 0.676 | 0.682 | 0.677 | 0.678 |

| 9_styles | 0.899 | 0.902 | 0.899 | 0.900 |

| 13_top_in_sector | 0.371 | 0.344 | 0.325 | 0.346 |

Single stocks are better diversifiers

create_avg_corr_table <- function(monthly_data, title = "Data Analysis") {

corr_matrix <- monthly_data$corr_matrix

symbols <- rownames(corr_matrix)

# average correlation for each stock excluding the stock itself

avg_correlations_per_stock <- map_dbl(seq_len(nrow(corr_matrix)), function(i) {

row_correlations <- corr_matrix[i, ]

mean(row_correlations[-i], na.rm = TRUE)

})

avg_correlations_df <- data.frame(symbol = symbols,

avg_correlation = avg_correlations_per_stock)

combined_data <- left_join(monthly_data$volatilities,

monthly_data$avg_returns, by = "symbol") |>

left_join(avg_correlations_df, by = "symbol")

gt_table <- combined_data |>

gt() |>

tab_header(title = title) |>

cols_label(

symbol = "Symbol",

volatility = "Volatility",

avg_return = "Avg Return",

avg_correlation = "Correlation(*)"

) |>

fmt_percent(columns = 2:3, decimals = 2) |>

fmt_number(columns = 4, decimals = 2) |>

tab_footnote("(*) Pairwise average(ρ): matrix row/column average excluding diagonal")

return(gt_table)

}

monthly_data <- stock_sets$analysis[[1]]$monthly

create_avg_corr_table(monthly_data, "Sectors, Monthly Returns")| Sectors, Monthly Returns | |||

|---|---|---|---|

| Symbol | Volatility | Avg Return | Correlation(*) |

| XLB | 5.30% | 0.73% | 0.76 |

| XLC | 6.09% | 0.58% | 0.69 |

| XLE | 8.35% | 0.40% | 0.54 |

| XLF | 5.44% | 0.87% | 0.72 |

| XLI | 5.12% | 0.91% | 0.77 |

| XLK | 5.17% | 1.50% | 0.69 |

| XLP | 3.64% | 0.72% | 0.66 |

| XLRE | 5.01% | 0.46% | 0.71 |

| XLU | 4.35% | 0.70% | 0.55 |

| XLV | 3.99% | 1.01% | 0.66 |

| XLY | 5.42% | 1.04% | 0.71 |

| (*) Pairwise average(ρ): matrix row/column average excluding diagonal | |||

monthly_data <- stock_sets$analysis[[3]]$monthly

create_avg_corr_table(monthly_data, "Largest Stock in Sector, Monthly Returns")| Largest Stock in Sector, Monthly Returns | |||

|---|---|---|---|

| Symbol | Volatility | Avg Return | Correlation(*) |

| AAPL | 8.06% | 1.85% | 0.35 |

| AMZN | 8.68% | 1.84% | 0.29 |

| BRK-B | 4.81% | 1.03% | 0.44 |

| CMCSA | 6.50% | 0.77% | 0.38 |

| LIN | 5.21% | 1.15% | 0.42 |

| LLY | 6.47% | 2.08% | 0.11 |

| LVMUY | 6.92% | 1.31% | 0.38 |

| NEE | 5.59% | 1.11% | 0.21 |

| NHYDY | 10.39% | 0.40% | 0.32 |

| PLD | 6.40% | 1.07% | 0.37 |

| UNP | 6.33% | 1.12% | 0.39 |

| WMT | 5.14% | 0.80% | 0.27 |

| XOM | 7.52% | 0.46% | 0.28 |

| (*) Pairwise average(ρ): matrix row/column average excluding diagonal | |||

Visualize Correlation

These step took me too long because I couldn’t wrestle corrplot/ggcorrplot to my ends. I tried various packages but finally settled on the corrr package due to its elegant/tidy construction; e.g., if you use ggplot, you can guess its parameters. As the authors write,

At first, a correlation data frame might seem like an unnecessary complexity compared to the traditional matrix. However, the purpose of corrr is to help use explore these correlations, not to do mathematical or statistical operations. Thus, by having the correlations in a data frame, we can make use of packages that help us work with data frames like dplyr, tidyr, ggplot2, and focus on using data pipelines

library(corrr)

colors_corr_plot <- colorRampPalette(c("firebrick3", "firebrick1", "yellow", "seagreen1", "seagreen4"))

plot_corr <- function(matrix, title) {

matrix_df <- as_cordf(matrix) |> shave()

matrix_df |> rplot(shape = 15, print_cor = TRUE,

colors = colors_corr_plot(5),

legend = FALSE) +

theme(axis.text.x = element_text(angle = 90, hjust = 1))

}

get_corr_matrices <- function(row_df){

analyze_this <- row_df |>

pull(analysis)

corr_daily_matrix <- analyze_this[[1]][["daily"]]$corr_matrix

corr_weekly_matrix <- analyze_this[[1]][["weekly"]]$corr_matrix

corr_monthly_matrix <- analyze_this[[1]][["monthly"]]$corr_matrix

return(list(

corr_daily_matrix = corr_daily_matrix,

corr_weekly_matrix = corr_weekly_matrix,

corr_monthly_matrix = corr_monthly_matrix

))

}

select_row_1 <- stock_sets |> filter(set_id == "9_styles")

three_matrices <- get_corr_matrices(select_row_1)

cp1 <- three_matrices$corr_daily_matrix |> plot_corr("9_styles, daily")

# cp2 <- three_matrices$corr_weekly_matrix |> plot_corr("9_styles, weekly")

cp3 <- three_matrices$corr_monthly_matrix |> plot_corr("9_styles, monthly")

select_row_2 <- stock_sets |> filter(set_id == "11_sectors")

three_matrices <- get_corr_matrices(select_row_2)

cp4 <- three_matrices$corr_daily_matrix |> plot_corr("11_sectors, daily") +

theme(legend.position = "right")

# cp5 <- three_matrices$corr_weekly_matrix |> plot_corr("11_sectors, weekly")

cp6 <- three_matrices$corr_monthly_matrix |> plot_corr("11_sectors, monthly") +

theme(legend.position = "right")

select_row_3 <- stock_sets |> filter(set_id == "13_top_in_sector")

three_matrices <- get_corr_matrices(select_row_3)

cp7 <- three_matrices$corr_daily_matrix |> plot_corr("13_top_in_sector, daily")

# cp8 <- three_matrices$corr_weekly_matrix |> plot_corr("13_top_in_sector, weekly")

cp9 <- three_matrices$corr_monthly_matrix |> plot_corr("13_top_in_sector, monthly")

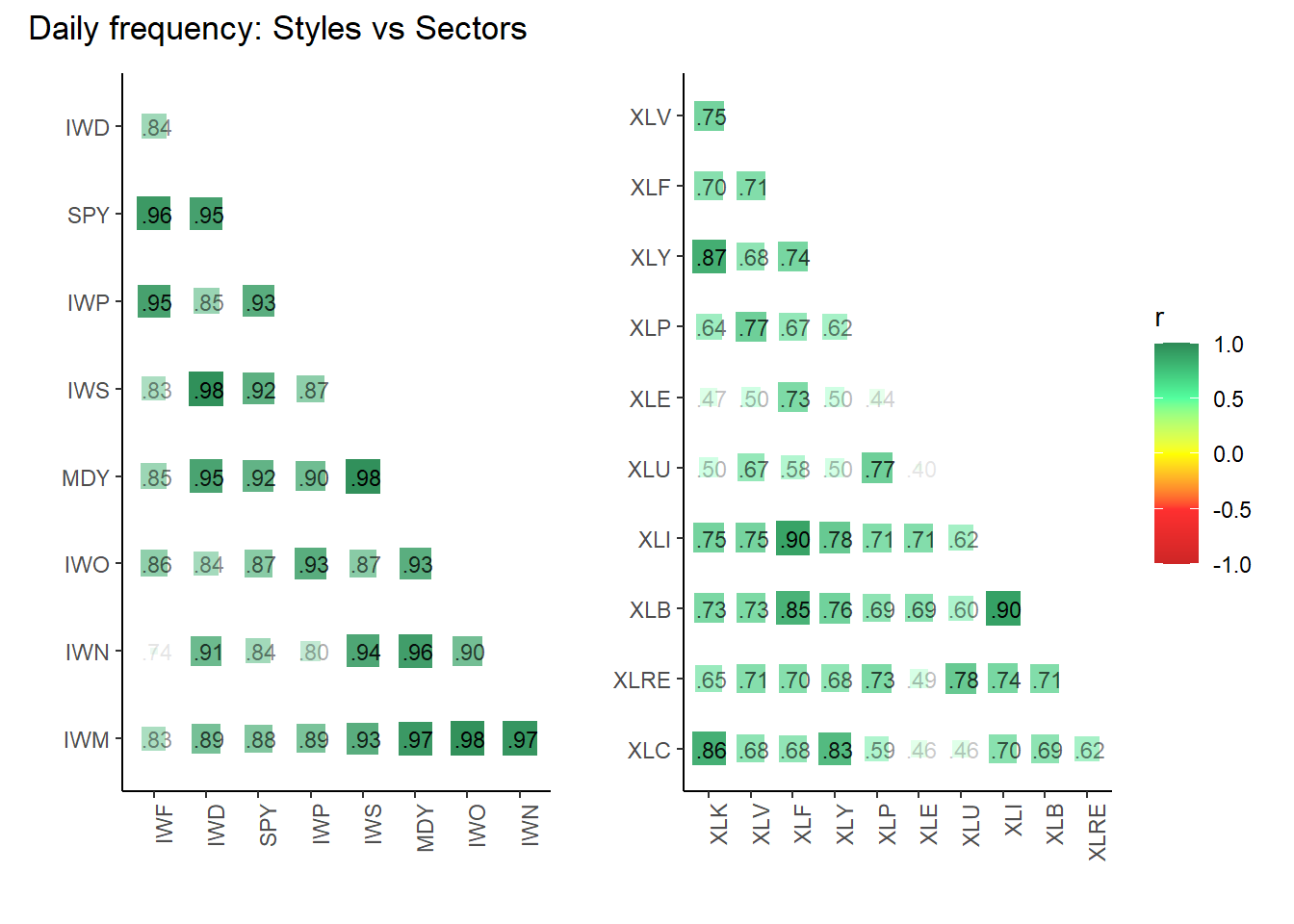

cp1 + cp4 + plot_annotation("Daily frequency: Styles vs Sectors")

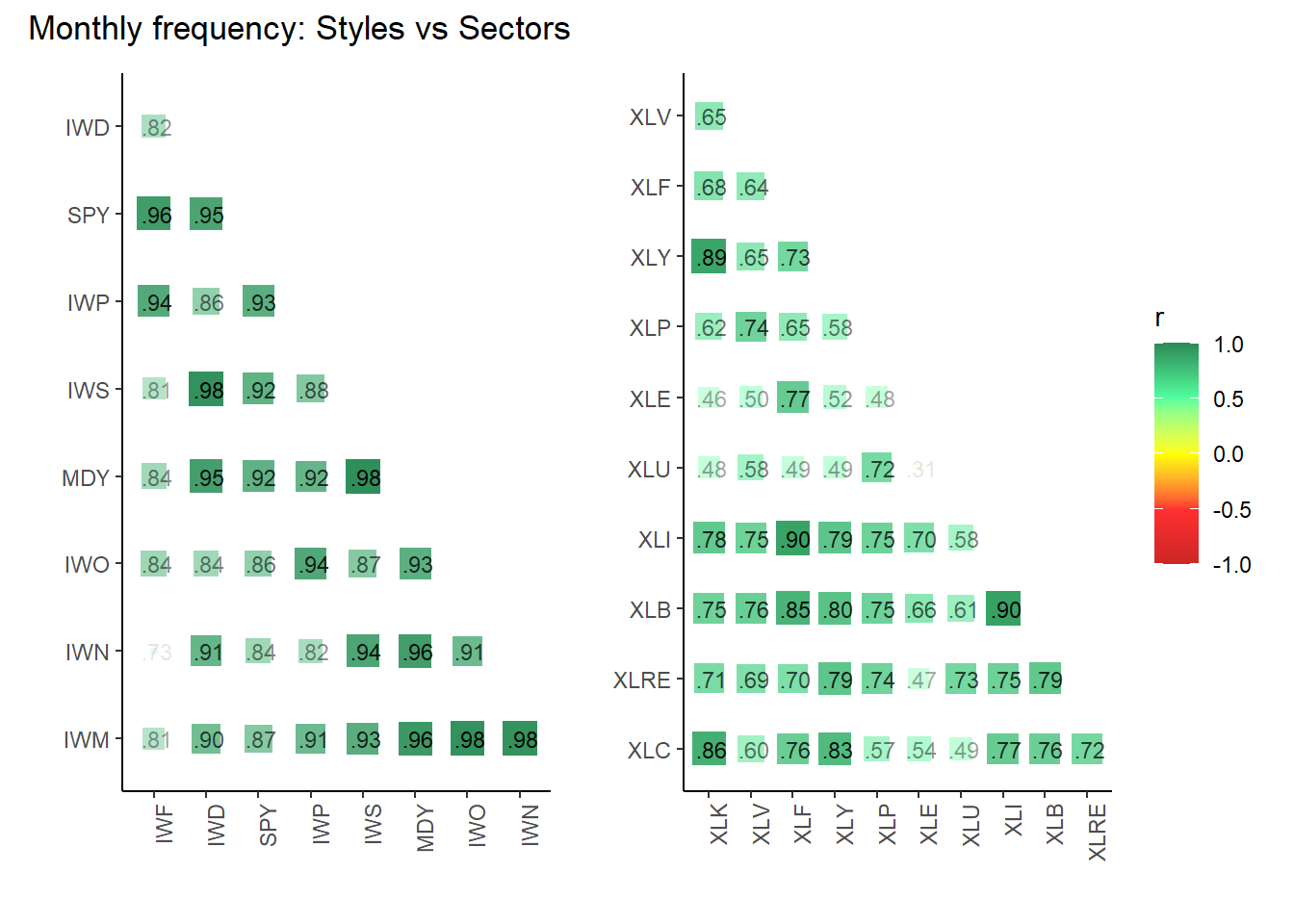

cp3 + cp6 + plot_annotation("Monthly frequency: Styles vs Sectors")

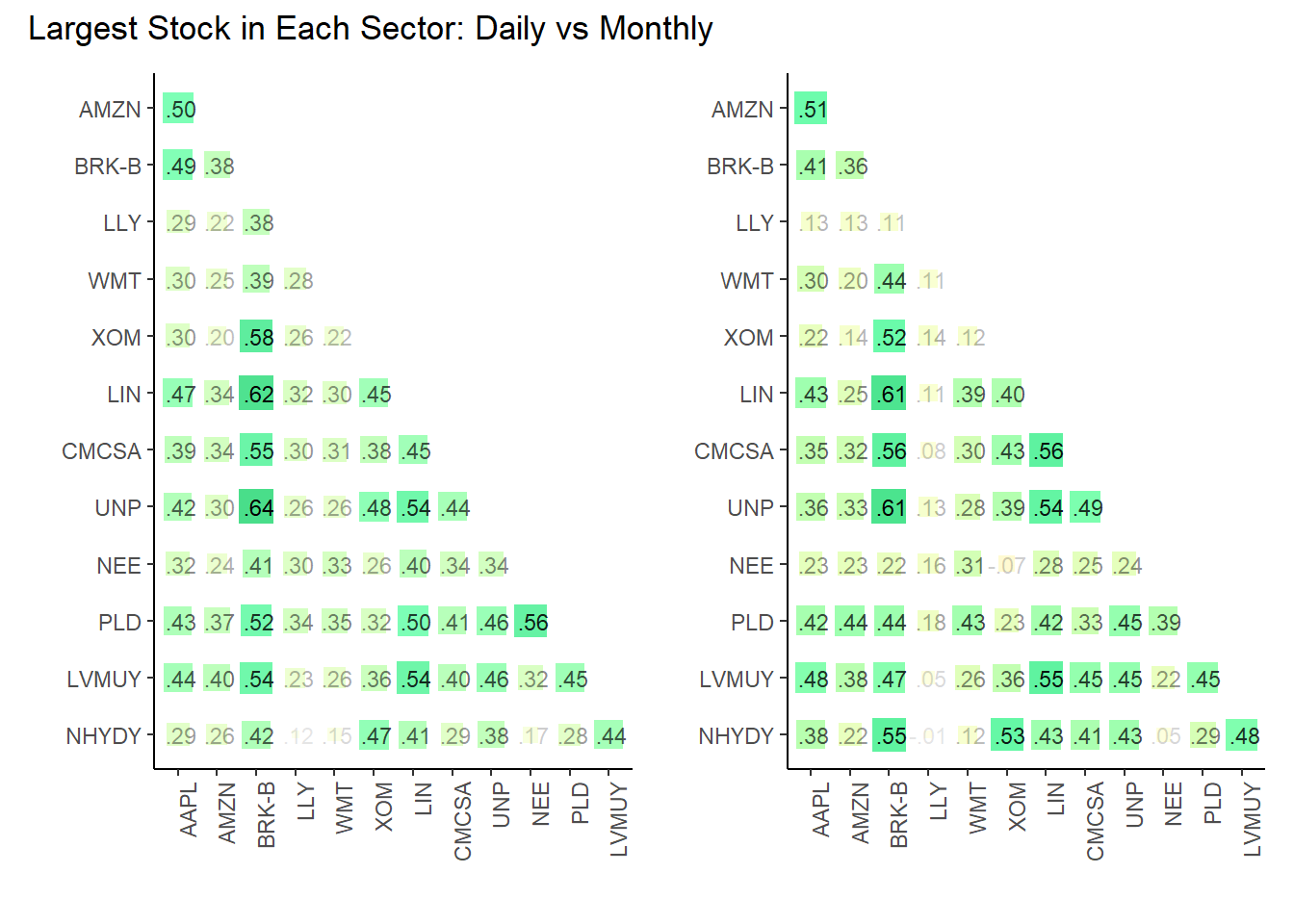

cp7 + cp9 + plot_annotation("Largest Stock in Each Sector: Daily vs Monthly")

Simulation

There are four steps here: select the portfolio, bias the random weights (if desired), setup the simulation, and run the simulation.

Simulation: 1. Select the portfolio (set of tickers/symbols)

# Selecting the desired set (e.g., "Set 1")

select_set <- stock_sets |>

filter(set_id == "11_sectors") |>

pull("analysis")

analyze_set <- select_set[[1]]

analyze_period <- analyze_set$monthly

# Extracting components from the selected set

exp_returns_period <- analyze_period$avg_returns$avg_return

names(exp_returns_period) <- analyze_period$avg_returns$symbol

volatilities_period <- analyze_period$volatilities$volatility

names(volatilities_period) <- analyze_period$volatilities$symbol

corr_matrix_period <- analyze_period$corr_matrix

num_stocks_period <- length(volatilities_period)Simulation: 2. Bias the random weights

This is an experiment to see if we can bias the random weights to get a better result. Rather than deduce a formula, I decided to ask, what is a more (or less) desirable feature of a diversifying asset? (in the mean-variance framework, it’s an asset with low marginal volatility). I decided to include the Sharpe ratio, expected utility (i.e., the expected rate of return minus half the risk aversion coeffient multiplied by the variance), and average correlation.

calculate_desirability <- function(exp_returns, volatilities, corr_matrix, A, risk_free_rate,

utility_weight, sharpe_weight, correlation_weight) {

# Calculate the variance as the square of volatility

variance <- volatilities^2

# Calculate the utility for each sector

utility <- exp_returns - 0.5 * A * variance

# Calculate the Sharpe ratio for each sector

sharpe_ratio <- (exp_returns - risk_free_rate) / volatilities

# Calculate the average correlation for each sector

avg_correlation <- apply(corr_matrix, 1, function(x) mean(x[-which(x == 1)], na.rm = TRUE))

write.matrix(corr_matrix, "avg_correlation.csv", sep = ",")

# Calculate the desirability score

desirability_score <- utility_weight * (utility * 100) +

sharpe_weight * (sharpe_ratio * 3 ) -

correlation_weight * avg_correlation # Negative because lower correlation is better

# Create a data frame for sector desirability

desirability_df <- data.frame(sector = names(exp_returns),

exp_returns = exp_returns,

volatilities = volatilities,

utility = utility,

sharpe_ratio = sharpe_ratio,

avg_correlation = avg_correlation,

desirability_score = desirability_score)

# Sort by desirability score

desirability_df <- desirability_df[order(-desirability_df$desirability_score),]

return(desirability_df)

}

# Example parameters

A <- 3 # Risk aversion coefficient

risk_free_rate <- 0.0 # Risk-free rate

utility_weight <- 0.3

sharpe_weight <- 0.4

correlation_weight <- 0.3

# Calculate desirability using the extracted components

sector_desirability <- calculate_desirability(exp_returns_period, volatilities_period, corr_matrix_period, A, risk_free_rate, utility_weight, sharpe_weight, correlation_weight)

sector_desirability |> gt() |>

cols_label(sector = "Ticker",

exp_returns = "Return",

volatilities = "Vol",

utility = "Utility",

sharpe_ratio = "Sharpe",

avg_correlation = "Avg Corr",

desirability_score = "Desirability") |>

fmt_percent(columns = 2:3) |>

fmt_number(columns = 4:7, decimals = 4)| Ticker | Return | Vol | Utility | Sharpe | Avg Corr | Desirability |

|---|---|---|---|---|---|---|

| XLK | 1.50% | 5.17% | 0.0110 | 0.2909 | 0.5422 | 0.5171 |

| XLV | 1.01% | 3.99% | 0.0077 | 0.2534 | 0.7093 | 0.3230 |

| XLP | 0.72% | 3.64% | 0.0052 | 0.1983 | 0.5484 | 0.2304 |

| XLY | 1.04% | 5.42% | 0.0060 | 0.1918 | 0.6908 | 0.2027 |

| XLI | 0.91% | 5.12% | 0.0052 | 0.1785 | 0.6589 | 0.1728 |

| XLF | 0.87% | 5.44% | 0.0042 | 0.1594 | 0.7085 | 0.1057 |

| XLU | 0.70% | 4.35% | 0.0042 | 0.1613 | 0.7629 | 0.0899 |

| XLB | 0.73% | 5.30% | 0.0031 | 0.1372 | 0.6885 | 0.0499 |

| XLC | 0.58% | 6.09% | 0.0003 | 0.0959 | 0.6580 | −0.0738 |

| XLRE | 0.46% | 5.01% | 0.0008 | 0.0919 | 0.7664 | −0.0944 |

| XLE | 0.40% | 8.35% | −0.0064 | 0.0483 | 0.7167 | −0.3499 |

Simulation: 3. Setup the simulation

The get_random_weights function returns a dataframe of random weights (that sum to 1). Each column is a set of weights for a single simulation.

This adds one innovation to the (my previous) naive approach. As previously, I still assume: the expected return for each stock is the average return for that stock over the entire period; the volatility for each stock is the average volatility for that stock over the entire period; and the correlation matrix (which obviously implies the covariance matrix) is computed from the pairwise (log) return vectors. In short, I’m assuming that the future will be like the past.

The innovation is that I bias the random weights to slightly favor the stocks with the highest “desirability” scores, as defined in the previous chunk. Desirability is just a weighted average of Utility, Sharpe ratio and (the inverse of) average correlation. Once random weights are selected, the portfolio return and volatility are calculated; and those don’t depend on the bias. The idea here is simply to (probably slightly) favor the simulation’s density toward the efficient segment.

# returns a data frame of random weights

# rows = weight per stock; columns = number of simulations

get_random_weights <- function(num_stocks, num_simulations, probabilities, row_names = NULL) {

set.seed(47391)

weights_df <- matrix(nrow = num_stocks, ncol = num_simulations)

for (i in 1:num_simulations) {

# Generate weights influenced by probabilities

weights <- runif(num_stocks) * probabilities

weights_df[, i] <- weights / sum(weights) # Normalize the weights

}

weights_df <- as.data.frame(weights_df)

if (!is.null(row_names) && length(row_names) == num_stocks) {

rownames(weights_df) <- row_names

}

return(weights_df)

}

# single simulation: given a set of weights, computes the expected return and volatility

port_sim <- function(exp_returns, volatilities, corr_matrix, weights) {

cov_matrix <- outer(volatilities, volatilities) * corr_matrix

port_variance <- t(weights) %*% cov_matrix %*% weights

port_exp_return <- sum(weights * exp_returns)

return(list(exp_returns = exp_returns,

volatilities = volatilities,

cov_matrix = cov_matrix,

corr_matrix = corr_matrix,

port_variance = port_variance,

port_exp_return = port_exp_return))

}

# runs a port_simulation for each column in the weights_df

run_sims <- function(exp_returns, volatilities, corr_matrix, weights_df) {

simulations <- map(1:ncol(weights_df), ~ {

weights_vector <- weights_df[, .x]

port_sim(exp_returns, volatilities, corr_matrix, weights_vector)

})

return(simulations)

}Simulation: 4. Run the simulation (on a single set)

num_sims <- 10000 # Set the number of simulations

sector_desirability$desirability_score <- pmax(sector_desirability$desirability_score, 0)

total_score <- sum(sector_desirability$desirability_score)

probabilities <- sector_desirability$desirability_score / total_score

names(probabilities) <- sector_desirability$sector

ordered_probabilities <- probabilities[names(exp_returns_period)]

row_symbols <- names(exp_returns_period)

random_weights_df_period <- get_random_weights(num_stocks_period, num_sims,

ordered_probabilities, row_names = row_symbols)

# View first 5 columns (= simulations/trials)

random_weights_df_period |> dplyr::select(1:5) V1 V2 V3 V4 V5

XLB 0.02904022 0.05416135 0.02778490 0.02113182 0.068640582

XLC 0.00000000 0.00000000 0.00000000 0.00000000 0.000000000

XLE 0.00000000 0.00000000 0.00000000 0.00000000 0.000000000

XLF 0.07715564 0.05391847 0.11792040 0.04413685 0.032498297

XLI 0.07038140 0.14379002 0.10358717 0.15823493 0.106281860

XLK 0.39217487 0.08140458 0.17201663 0.24347196 0.290418025

XLP 0.10247948 0.30004556 0.16088140 0.19679704 0.079391443

XLRE 0.00000000 0.00000000 0.00000000 0.00000000 0.000000000

XLU 0.01658246 0.08766279 0.13995496 0.01986227 0.006779211

XLV 0.23783284 0.04282421 0.04622476 0.22763656 0.189368775

XLY 0.07435309 0.23619302 0.23162977 0.08872856 0.226621805sim_results_period <- run_sims(exp_returns_period,

volatilities_period,

corr_matrix_period,

random_weights_df_period)

# Testing

# print(sim_results_period[[1]])

results_df_period <- map_dfr(sim_results_period, ~ data.frame(Exp_Return = .x$port_exp_return,

Std_Dev = sqrt(.x$port_variance)))

# Define the risk-free rate

risk_free_cml_1 <- 0

risk_free_cml_2 <- 0.005

# Calculate the Sharpe Ratio for each simulation

results_df_period <- results_df_period |>

mutate(

Sharpe_Ratio_1 = (Exp_Return - risk_free_cml_1) / Std_Dev,

Sharpe_Ratio_2 = (Exp_Return - risk_free_cml_2) / Std_Dev

)

# Find the row with the highest Sharpe Ratio

best_sim_1 <- results_df_period[which.max(results_df_period$Sharpe_Ratio_1), ]

best_sim_2 <- results_df_period[which.max(results_df_period$Sharpe_Ratio_2), ]

# Print the best simulation result

print(best_sim_1) Exp_Return Std_Dev Sharpe_Ratio_1 Sharpe_Ratio_2

5333 0.01181061 0.03765077 0.3136885 0.1808891print(best_sim_2) Exp_Return Std_Dev Sharpe_Ratio_1 Sharpe_Ratio_2

6340 0.0129082 0.04164321 0.3099714 0.1899038# View summarized results for daily returns

print(head(results_df_period)) Exp_Return Std_Dev Sharpe_Ratio_1 Sharpe_Ratio_2

1 0.011451646 0.03877509 0.2953351 0.1663864

2 0.009070019 0.03843242 0.2359992 0.1059007

3 0.009775922 0.03997072 0.2445771 0.1194855

4 0.010426930 0.03721517 0.2801795 0.1458257

5 0.011009263 0.03991819 0.2757956 0.1505394

6 0.011803124 0.04004291 0.2947619 0.1698958Visualize the results

library(patchwork)

results_df <- results_df_period # continuity from prior

results_df <- results_df |>

arrange(Std_Dev) |>

mutate(is_efficient = Exp_Return >= cummax(Exp_Return))

efficient_portfolios <- results_df |>

arrange(Std_Dev) |>

mutate(cummax_return = cummax(Exp_Return)) |>

filter(Exp_Return >= cummax_return)

efficient_model <- lm(Exp_Return ~ poly(Std_Dev, 2), data = efficient_portfolios)

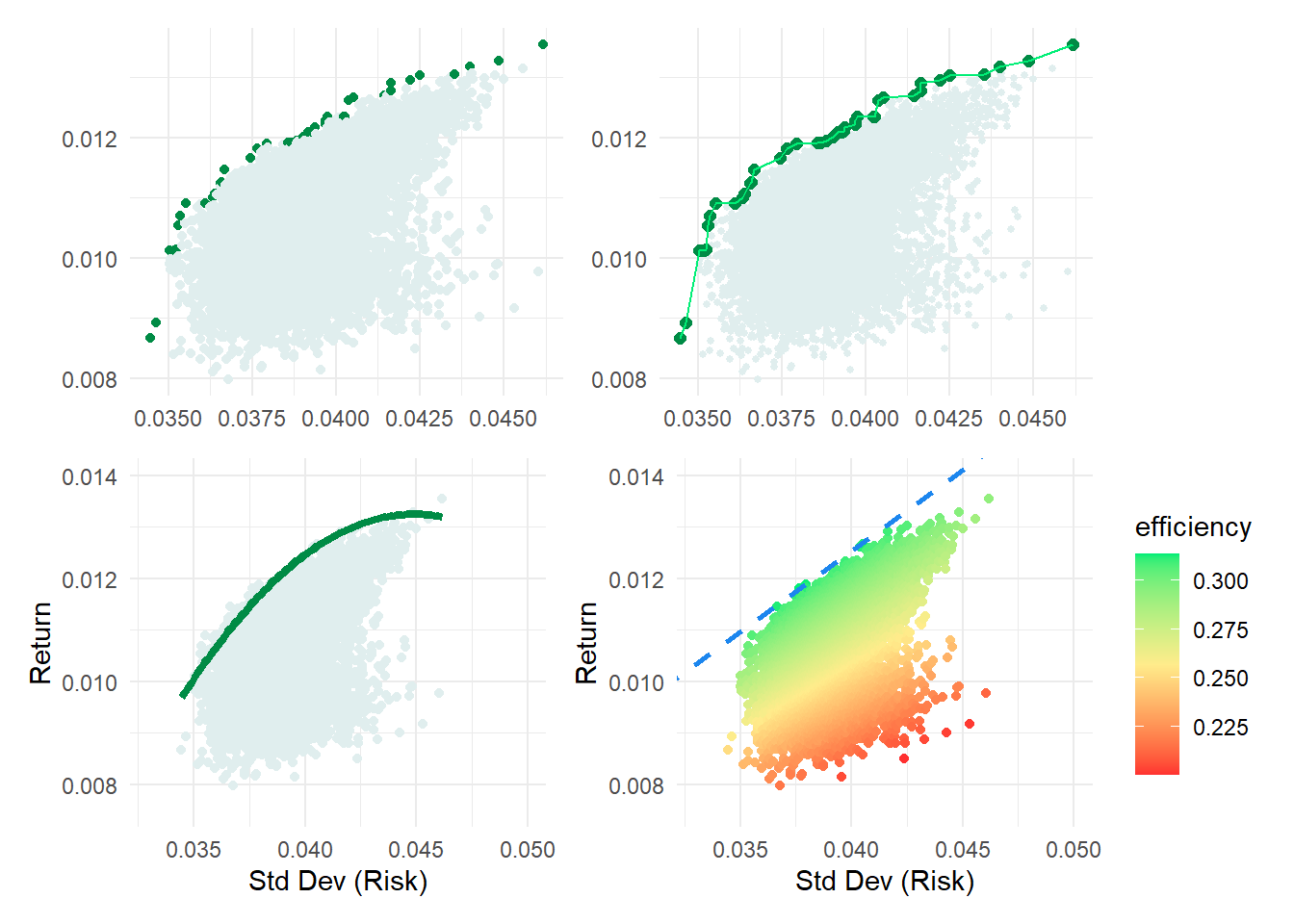

p1 <- ggplot(results_df, aes(x = Std_Dev, y = Exp_Return, color = is_efficient)) +

geom_point() +

scale_color_manual(values = c("azure2", "springgreen4")) +

theme_minimal() +

theme(

axis.title = element_blank(),

legend.position = "none"

)

p2 <- ggplot(results_df, aes(x = Std_Dev, y = Exp_Return)) +

geom_point(aes(color = is_efficient), size = 1) + # Default size for all points

geom_point(data = filter(results_df, is_efficient),

aes(color = is_efficient), size = 2) + # Larger size for efficient points

scale_color_manual(values = c("azure2", "springgreen4")) +

theme_minimal() +

geom_line(data = efficient_portfolios, aes(x = Std_Dev, y = Exp_Return), colour = "springgreen2") +

theme(

axis.title = element_blank(),

legend.position = "none"

)

p3 <- ggplot(results_df, aes(x = Std_Dev, y = Exp_Return)) +

geom_point(color = "azure2") +

geom_smooth(data = efficient_portfolios, method = "lm", formula = y ~ poly(x, 2),

se = FALSE, colour = "springgreen4", linewidth = 1.5) +

labs(x = "Std Dev (Risk)",

y = "Return") +

coord_cartesian(xlim = c(0.0330, 0.050), ylim = c(0.0075, 0.0140)) +

theme_minimal()

# Calculate a metric, Sharpe, that can inform COLOR fill

# ... but it will only be based on the first risk-free rate!

results_df <- results_df %>%

mutate(efficiency = (Exp_Return - risk_free_cml_1)/ Std_Dev)

slope_cml_1 <- (best_sim_1$Exp_Return - risk_free_cml_1) / best_sim_1$Std_Dev

slope_cml_2 <- (best_sim_2$Exp_Return - risk_free_cml_2) / best_sim_2$Std_Dev

extended_std_dev <- max(results_df_period$Std_Dev) * 1.2 # For example, 20% beyond the max std dev in the data

extended_exp_return_1 <- risk_free_cml_1 + slope_cml_1 * extended_std_dev

extended_exp_return_2 <- risk_free_cml_2 + slope_cml_2 * extended_std_dev

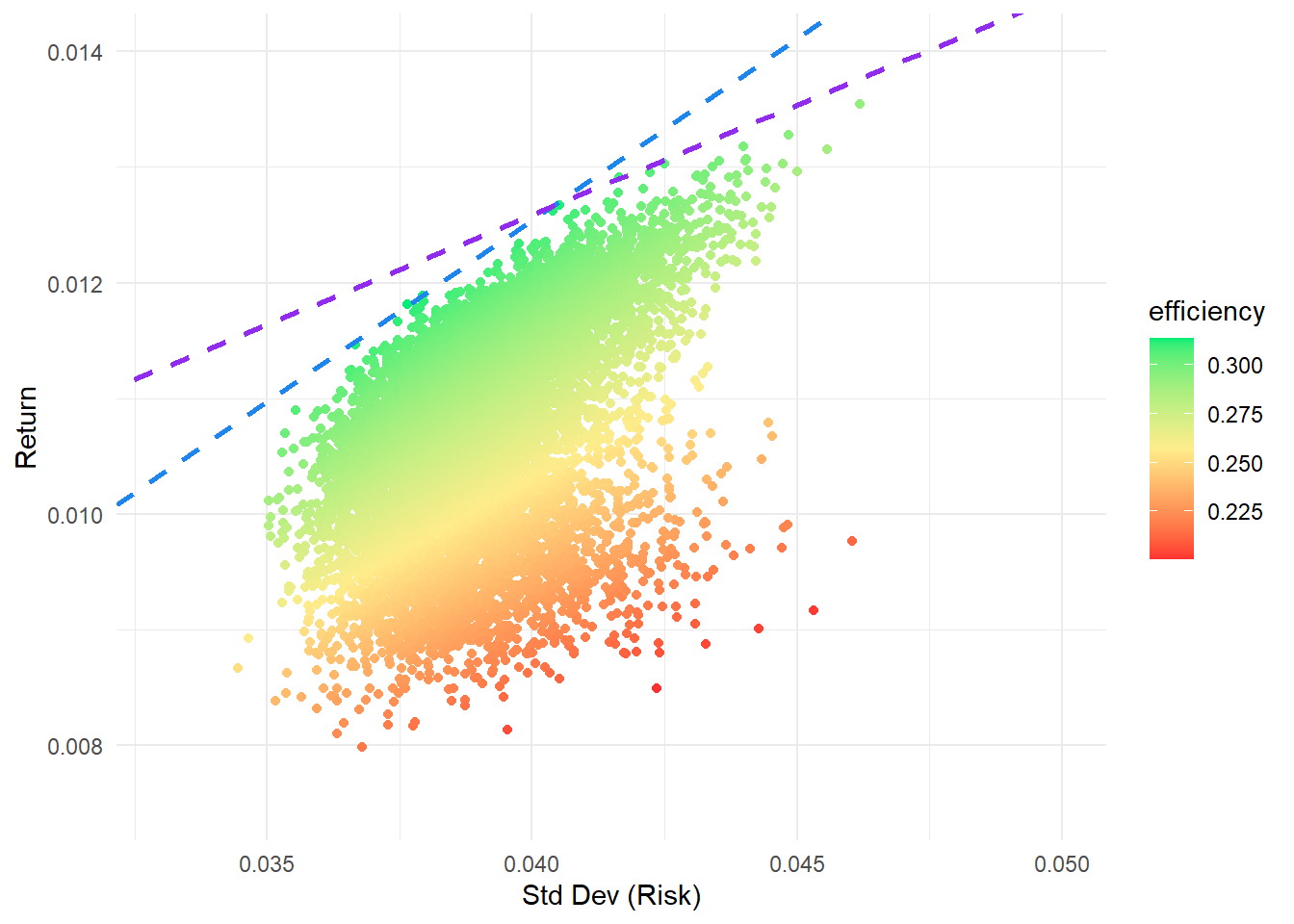

p4 <- ggplot(results_df, aes(x = Std_Dev, y = Exp_Return, color = efficiency)) +

geom_point() +

scale_color_gradientn(colors = c("firebrick1", "lightgoldenrod1", "springgreen2"),

values = scales::rescale(c(min(results_df$efficiency),

max(results_df$efficiency)))) +

geom_segment(aes(x = 0, y = risk_free_cml_1, xend = extended_std_dev, yend = extended_exp_return_1),

color = "dodgerblue2", linetype = "dashed", linewidth = 1) +

theme_minimal() +

coord_cartesian(xlim = c(0.0330, 0.050), ylim = c(0.0075, 0.0140)) +

labs(x = "Std Dev (Risk)",

y = "Return",

color = "efficiency")

(p1 + p2) / (p3 + p4 )

Add the second CML

p5 <- p4 + geom_segment(aes(x = 0, y = risk_free_cml_2, xend = extended_std_dev, yend = extended_exp_return_2),

color = "purple2", linetype = "dashed", linewidth = 1)

p5

This is for the social thumb

cp9_thumb <- cp9 + theme(legend.position = "right")

(cp7 + cp9_thumb) / (p2 + p4)