library(tidyverse)

library(corrplot); library(ggcorrplot) # may not use

library(factoextra)

# source is free trial of S&P https://www.tiingo.com/

# This is approximately the S&P1500; i.e, large-, mid- and small-cap stocks

stocks1500 <- read_csv("k-means-set_v1_2.csv")

stocks1500 <- stocks1500 |> rename(

market_cap = 'Market Cap',

div_yield = 'Dividend Yield',

gross_margin = 'Gross Margin',

revenue_growth = 'Revenue Growth (QoQ)',

rho_sp500 = 'Correlation to S&P 500',

volatility = '1 Year Volatility',

pe_ratio = 'P/E Ratio',

debt_equity = 'Debt/Equity (D/E) Ratio',

ROE = 'Return on Equity (ROE)',

ROA = 'Return on Assets (ROA/ROI)',

TSR_1year = '1 Year Return',

rho_treasury = 'Correlation to U.S. Treasuries',

enterprise_value = 'Enterprise Val',

pb_ratio = 'P/B Ratio'

)

# remove outliers, observed ex post

stocks1500 <- stocks1500 |> filter(Ticker != "AMZN")

stocks1500 <- stocks1500 |> filter(!Ticker %in% c("PDD", "MELI", "NDAQ", "RCL"))

# filtering by market cap: important reduction here!

df <- stocks1500 |> filter(market_cap > mean(stocks1500$market_cap))

numeric_cols <- df |> select_if(is.numeric)

options(scipen = 999)

# because we're going to standardize the features

original_means <- colMeans(numeric_cols)

original_sds <- numeric_cols |> map_dbl(sd)

std_cols <- numeric_cols |>

mutate(across(everything(), ~(. - mean(.)) / sd(.)))

df_std <- df |>

select(Ticker, Name, Sector, Industry) |>

bind_cols(std_cols)Contents

- Retrieve stocks and standardize features

- Select features

- Elbow method for optimal clusters

- K-means clusters

- Visualized

- Unscaled centroids

Retrive stocks and standardize features

Select features

selected_features <- c("volatility", "TSR_1year")Elbow method for optimal clusters

compute_elbow <- function(df, selected_columns) {

numeric_data <- select(df, all_of(selected_columns))

compute_wss <- function(k) {

kmeans_result <- kmeans(numeric_data, centers = k, nstart = 25)

kmeans_result$tot.withinss

}

k_values <- 1:25

wss_values <- map_dbl(k_values, compute_wss)

elbow_data <- tibble(k = k_values, wss = wss_values)

# Calculate slopes

elbow_data <- elbow_data %>%

mutate(slope = c(NA, diff(wss) / diff(k)))

return(elbow_data)

}

elbow_data <- compute_elbow(df_std, selected_features)

plot_elbow <- function(elbow_data) {

ggplot(elbow_data, aes(x = k, y = wss)) +

geom_line() +

geom_point() +

geom_text(aes(label = round(slope, 1)), vjust = -1.5) +

theme_minimal() +

labs(title = "Elbow Method for Optimal Number of Clusters",

x = "Number of Clusters (k)",

y = "Total Within-Cluster Sum of Squares")

}

# Use the function with your data

elbow_plot <- plot_elbow(elbow_data)

# Display the plot

print(elbow_plot)

K-means clusters

set.seed(9367) # Set a random seed for reproducibility

# Color palette

# location (ex post): top-middle, bottom-middle, bottom-right, left, top-right

custom_colors <- c("blue1", "darkorange1", "firebrick3", "cyan3", "springgreen3")

numeric_data <- df_std |> select(all_of(selected_features))

# based on the elbow method's so-called

# elbow point but ultimately is discretionary

num_clusters <- 5

kmeans_result_n <- kmeans(numeric_data, centers = num_clusters, nstart = 25)

# Print out the results

print(kmeans_result_n)K-means clustering with 5 clusters of sizes 68, 69, 30, 85, 30

Cluster means:

volatility TSR_1year

1 -0.1663365 0.6846281

2 0.0751603 -0.6467280

3 1.7067078 -0.1904547

4 -0.9749478 -0.6417393

5 1.2598050 1.9443669

Clustering vector:

[1] 1 5 1 1 1 4 1 4 2 4 5 1 4 5 3 2 1 1 4 4 4 2 4 1 4 1 4 1 2 2 4 1 2 1 2 2 2

[38] 5 2 4 1 3 4 4 2 3 4 1 2 2 5 4 2 2 5 2 4 4 2 2 4 4 2 1 2 4 2 1 2 4 4 2 2 4

[75] 2 2 4 5 1 5 4 2 4 1 5 4 4 4 2 5 1 2 4 4 1 5 4 4 2 4 1 4 1 1 5 2 5 2 1 3 1

[112] 4 3 3 4 2 2 4 4 4 4 5 4 2 1 5 5 4 4 5 1 3 2 1 4 1 2 4 1 1 2 1 1 3 4 1 1 1

[149] 3 3 3 1 2 3 5 1 4 1 1 4 2 4 1 5 1 4 2 4 1 3 2 4 3 2 3 4 1 2 3 3 1 4 4 3 4

[186] 5 1 3 2 2 3 3 3 1 1 2 4 3 4 2 2 4 1 4 2 4 4 2 4 4 4 5 1 1 2 2 2 2 4 4 3 1

[223] 4 3 1 1 4 1 3 1 5 3 1 3 4 2 2 1 5 5 4 5 4 4 2 2 4 2 1 1 2 2 4 4 4 2 3 1 5

[260] 1 2 1 2 1 4 3 2 1 5 1 5 4 2 5 2 4 2 5 4 4 1 4

Within cluster sum of squares by cluster:

[1] 29.48504 27.95429 21.43397 27.33563 27.48363

(between_SS / total_SS = 76.2 %)

Available components:

[1] "cluster" "centers" "totss" "withinss" "tot.withinss"

[6] "betweenss" "size" "iter" "ifault" # attach cluster membership back to the original data

df_std$cluster <- kmeans_result_n$cluster

df$cluster <- kmeans_result_n$cluster

# Calculate mean and standard deviation for each feature, grouped by cluster

cluster_summary <- df |>

group_by(cluster) |>

summarise(across(everything(),

list(mean = ~mean(.), sd = ~sd(.)),

.names = "{.col}_{.fn}"))

# View the results: below instead

# cluster_summary$volatility_mean

# cluster_summary$volatility_sd

# cluster_summary$TSR_1year_mean

# cluster_summary$TSR_1year_sd

# cross_tab <- table(df_std$Sector, kmeans_result_n$cluster)

table(df_std$Sector, kmeans_result_n$cluster)

1 2 3 4 5

Basic Materials 6 4 3 1 2

Communication Services 3 3 0 3 0

Consumer Cyclical 4 2 4 0 4

Consumer Defensive 2 8 1 13 0

Discretionary 0 1 0 0 0

Energy 9 4 13 4 2

Financial Services 12 18 3 10 7

Healthcare 3 4 0 17 1

Industrials 14 8 0 17 4

Real Estate 3 4 0 3 0

Technology 10 7 6 3 10

Unknown 1 0 0 1 0

Unknown Sector 1 3 0 1 0

Utilities 0 3 0 12 0Visualized

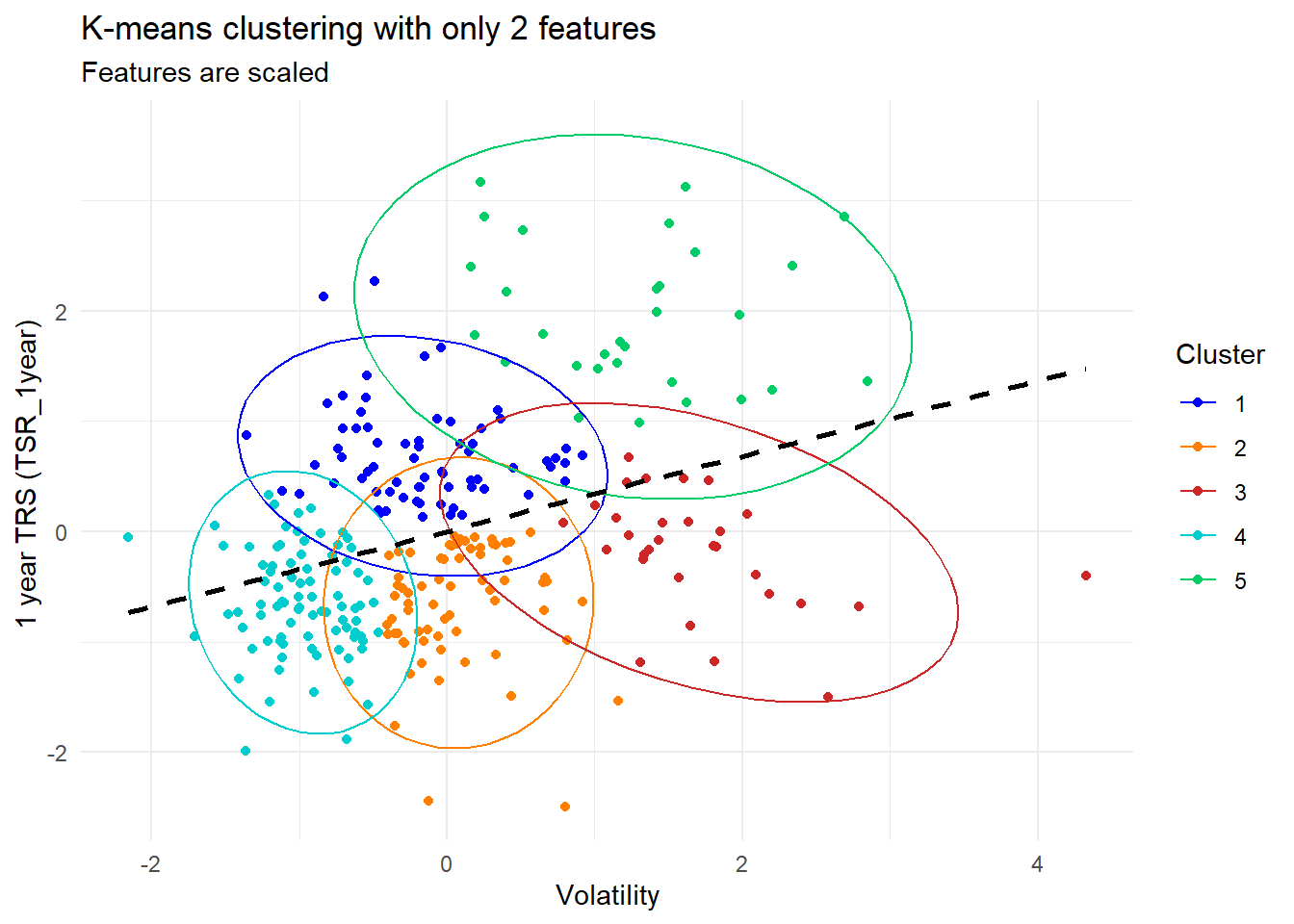

# Plotting

ggplot(df_std, aes(x = volatility, y = TSR_1year, color = as.factor(cluster))) +

geom_point() + # Add points

stat_ellipse(type = "norm", level = 0.95) +

geom_smooth(method = "lm", se = FALSE, color = "black", linetype = "dashed") +

scale_color_manual(values = custom_colors) + # Use custom color palette

theme_minimal() + # Minimal theme

labs(color = "Cluster",

title = "K-means clustering with only 2 features",

subtitle = "Features are scaled",

x = "Volatility",

y = "1 year TRS (TSR_1year) ")

model_lm <- lm(TSR_1year ~ volatility, data = df_std)

corr <- cor(df_std$TSR_1year, df_std$volatility)Unscaled centroids

selected_means <- original_means[selected_features]

selected_sds <- original_sds[selected_features]

scaled_centroids <- kmeans_result_n$centers

# Element-wise multiplication of each column by the corresponding standard deviation

# Then, addition of each column by the corresponding mean

unscaled_centroids <- sweep(scaled_centroids, 2, selected_sds, FUN = "*")

unscaled_centroids <- sweep(unscaled_centroids, 2, selected_means, FUN = "+")

unscaled_centroids_df <- as.data.frame(unscaled_centroids)

rownames(unscaled_centroids_df) <- paste("Cluster", 1:nrow(unscaled_centroids_df))

# sort by volatility

unscaled_centroids_df <- unscaled_centroids_df[order(unscaled_centroids_df$volatility), ]

print(unscaled_centroids_df) volatility TSR_1year

Cluster 4 0.2438719 -0.04716554

Cluster 1 0.3173974 0.26064020

Cluster 2 0.3393562 -0.04832325

Cluster 5 0.4470738 0.55298364

Cluster 3 0.4877098 0.05756260