my_libraries <- c("C50", "gmodels", "tidyverse", "openxlsx",

"rattle", "rpart", "rpart.plot")

lapply(my_libraries, library, character.only = TRUE)Contents

- Train (and graph) dividend payer with rpart(), rpart.plot and C5.0

- Loan default train

- Loan default prediction

- Adding penalty matrix to make false negatives costly

- Trees are random but not too fragile

To write a PQ set for decision trees, I experimented below. First the libraries:

Predicting dividend

GARP’s motivating example is a super simple (n = 20) dataset of public companies the either pay or do not pay a Dividend. The my20firms dataframe (you can see) is slightly altered to achieve a tree that I liked better for purposes of a practice question:

# my20firms <- garp_data

# my20firms$Dividend[1] <- 0

# my20firms$Dividend[9] <- 0

# my20firms$Dividend[12] <- 1

# my20firms$Dividend[13] <- 0

# my20firms$Dividend[15] <- 0

# colnames(my20firms)[colnames(my20firms) == "Retail_investor"] <- "Retail"

# colnames(my20firms)[colnames(my20firms) == "Large_cap"] <- "LargeCap"

# write.xlsx(my20firms, file = "dividendExampleModified_v3.xlsx")

# my20firms <- read.xlsx("dividendExampleModified_v3.xlsx")

# saveRDS(my20firms, file = "my20firms-rds.RDS")

my20firms <- readRDS("my20firms-rds.RDS")

my20firms Dividend Earnings LargeCap Retail Tech

1 0 0 1 40 1

2 1 1 1 30 0

3 1 1 1 20 0

4 0 0 0 80 1

5 1 0 1 20 0

6 0 1 0 30 1

7 0 1 0 40 0

8 1 0 1 60 0

9 0 1 1 20 1

10 0 1 1 40 0

11 0 0 0 20 1

12 1 0 1 70 0

13 0 1 0 30 1

14 1 0 1 70 0

15 0 0 1 50 1

16 1 0 1 60 1

17 1 1 1 30 0

18 0 1 0 30 1

19 0 0 0 40 0

20 1 1 1 50 0fit2 <- rpart(Dividend ~ ., data = my20firms,

parms = list(split = "gini"),

control = rpart.control(minsplit = 1,

minbucket = 1,

maxdepth = 4))

# summary(fit2) printout is too long

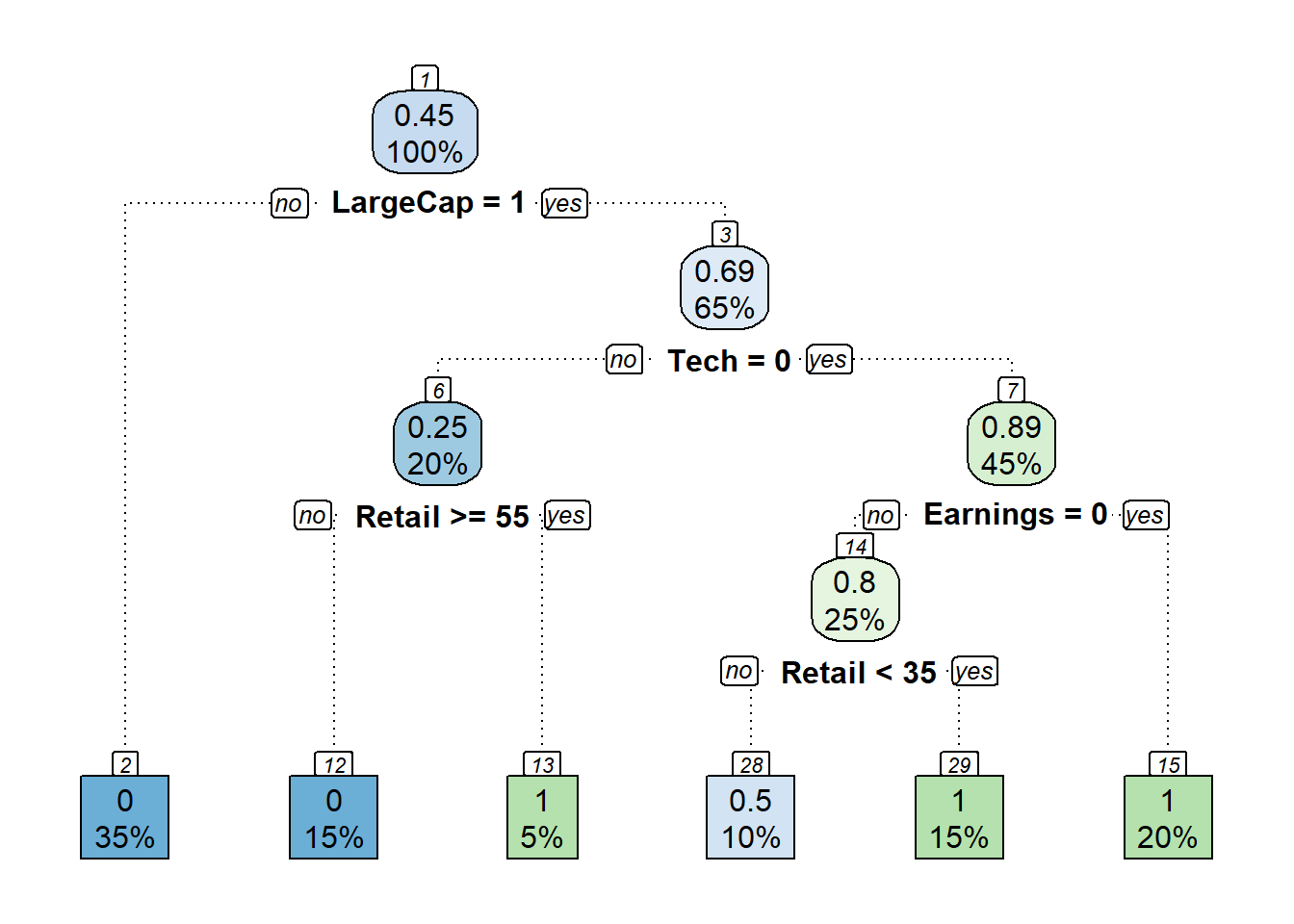

print(fit2)n= 20

node), split, n, deviance, yval

* denotes terminal node

1) root 20 4.9500000 0.4500000

2) LargeCap< 0.5 7 0.0000000 0.0000000 *

3) LargeCap>=0.5 13 2.7692310 0.6923077

6) Tech>=0.5 4 0.7500000 0.2500000

12) Retail< 55 3 0.0000000 0.0000000 *

13) Retail>=55 1 0.0000000 1.0000000 *

7) Tech< 0.5 9 0.8888889 0.8888889

14) Earnings>=0.5 5 0.8000000 0.8000000

28) Retail>=35 2 0.5000000 0.5000000 *

29) Retail< 35 3 0.0000000 1.0000000 *

15) Earnings< 0.5 4 0.0000000 1.0000000 *printcp(fit2)

Regression tree:

rpart(formula = Dividend ~ ., data = my20firms, parms = list(split = "gini"),

control = rpart.control(minsplit = 1, minbucket = 1, maxdepth = 4))

Variables actually used in tree construction:

[1] Earnings LargeCap Retail Tech

Root node error: 4.95/20 = 0.2475

n= 20

CP nsplit rel error xerror xstd

1 0.440559 0 1.00000 1.11610 0.056479

2 0.228352 1 0.55944 1.12013 0.298518

3 0.151515 2 0.33109 1.04063 0.309021

4 0.039282 3 0.17957 0.81948 0.360160

5 0.010000 5 0.10101 0.80808 0.361385rpart.plot(fit2, yesno = 2, left=FALSE, type=2, branch.lty = 3, nn= TRUE,

box.palette = "BuGn", leaf.round=0)

# converting the target to factor

my20firms$Dividend <- as_factor(my20firms$Dividend)

fit3 <- rpart(Dividend ~ ., data = my20firms,

parms = list(split = "gini"),

control = rpart.control(minsplit = 1,

minbucket = 1,

maxdepth = 4))

print(fit3)n= 20

node), split, n, loss, yval, (yprob)

* denotes terminal node

1) root 20 9 0 (0.5500000 0.4500000)

2) LargeCap< 0.5 7 0 0 (1.0000000 0.0000000) *

3) LargeCap>=0.5 13 4 1 (0.3076923 0.6923077)

6) Tech>=0.5 4 1 0 (0.7500000 0.2500000)

12) Retail< 55 3 0 0 (1.0000000 0.0000000) *

13) Retail>=55 1 0 1 (0.0000000 1.0000000) *

7) Tech< 0.5 9 1 1 (0.1111111 0.8888889) *rpart.plot(fit3, yesno = 2, left=FALSE, type=2, branch.lty = 3, nn= TRUE,

box.palette = "BuGn", leaf.round=0)

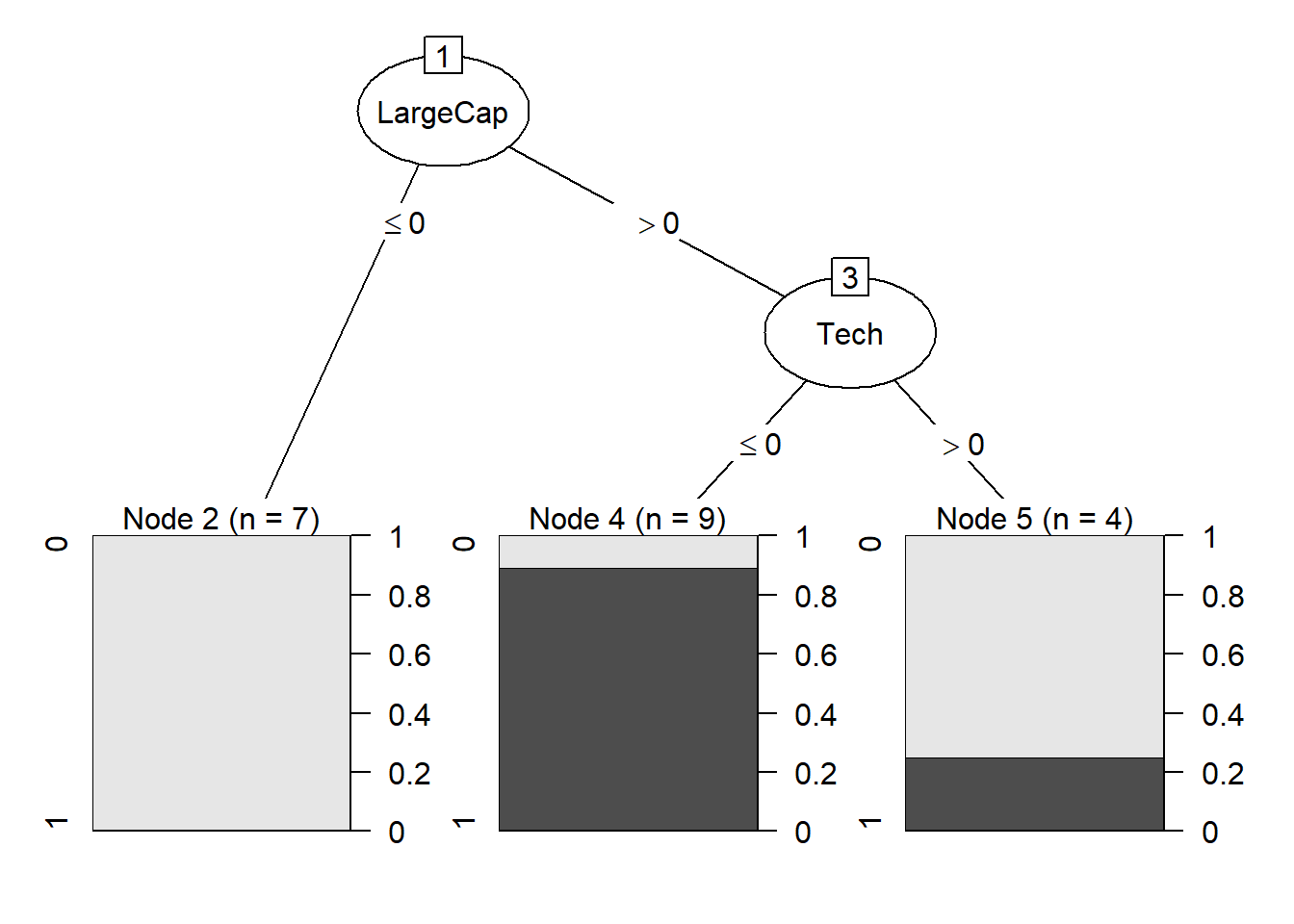

I had to refresh my knowledge of decision trees, and for that I depended on the awesome book () that I will review in the future (almost done!). He uses C5.0 algorithm (per the C50 package) and I just wanted to see its defaults:

tree_c5 <- C5.0(Dividend ~ ., data = my20firms)

plot(tree_c5)

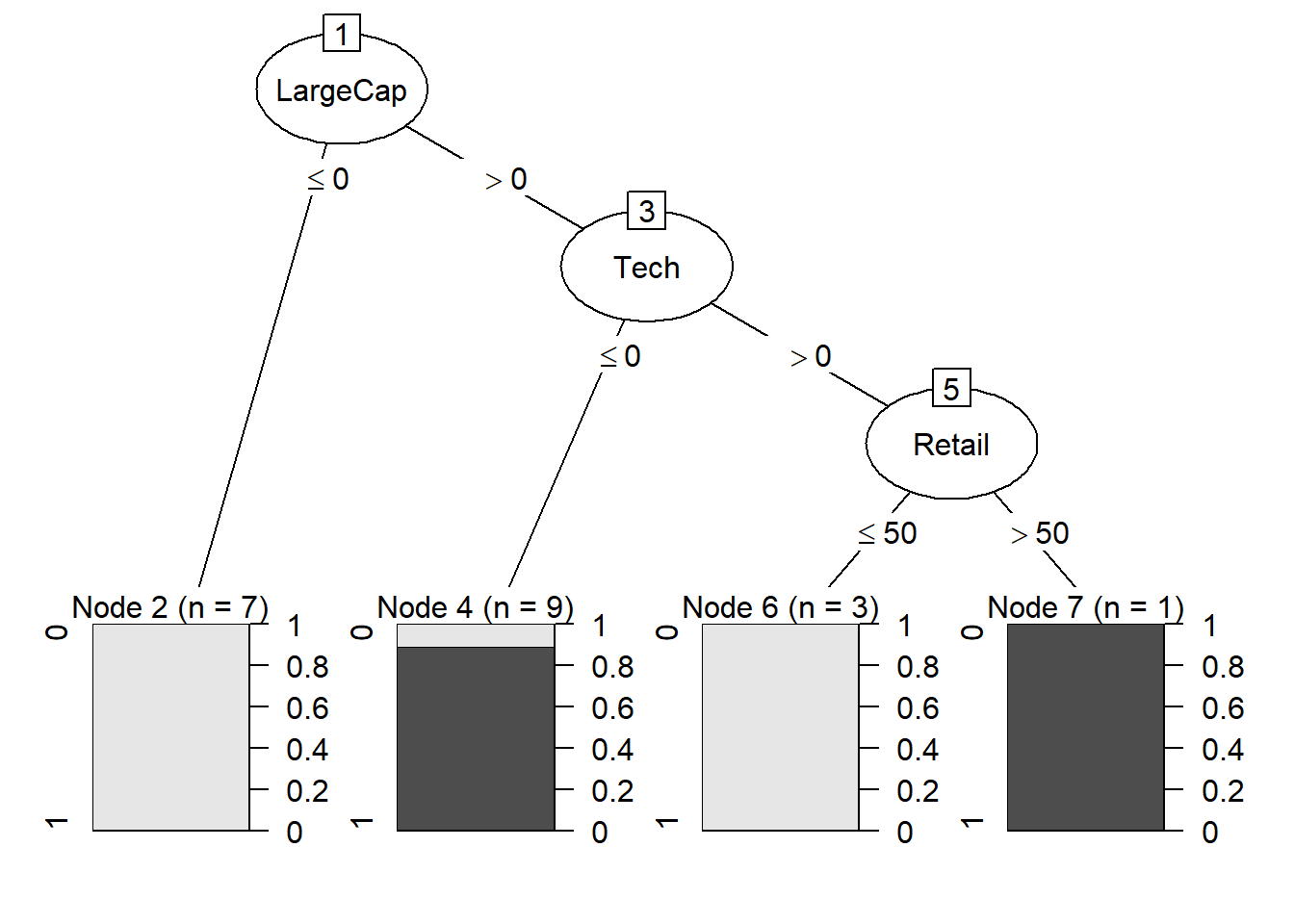

# set MinCases = 1

tree_c5_v2 <- C5.0(Dividend ~ .,

control = C5.0Control(minCases = 1),

data = my20firms)

plot(tree_c5_v2)

Loan default examples

Now I will switch datasets, and use the same loan default dataset used in the book. But I will use the more familiar rpart() function to train the tree. The result is similar but not identical (and please not the difference is not due to sampling varation: my test sample is the same).

set.seed(9829)

train_sample <- sample(1000, 900)

credit <- read.csv("credit.csv", stringsAsFactors = TRUE)

# split the data frames

credit_train <- credit[train_sample, ]

credit_test <- credit[-train_sample, ]

credit_train$credit_history <- credit_train$credit_history |>

fct_relevel("critical", "poor", "good", "very good", "perfect")

tree_credit_train <- rpart(default ~ ., data = credit_train,

parms = list(split = "gini"),

control = rpart.control(minsplit = 1,

minbucket = 1,

maxdepth = 4))

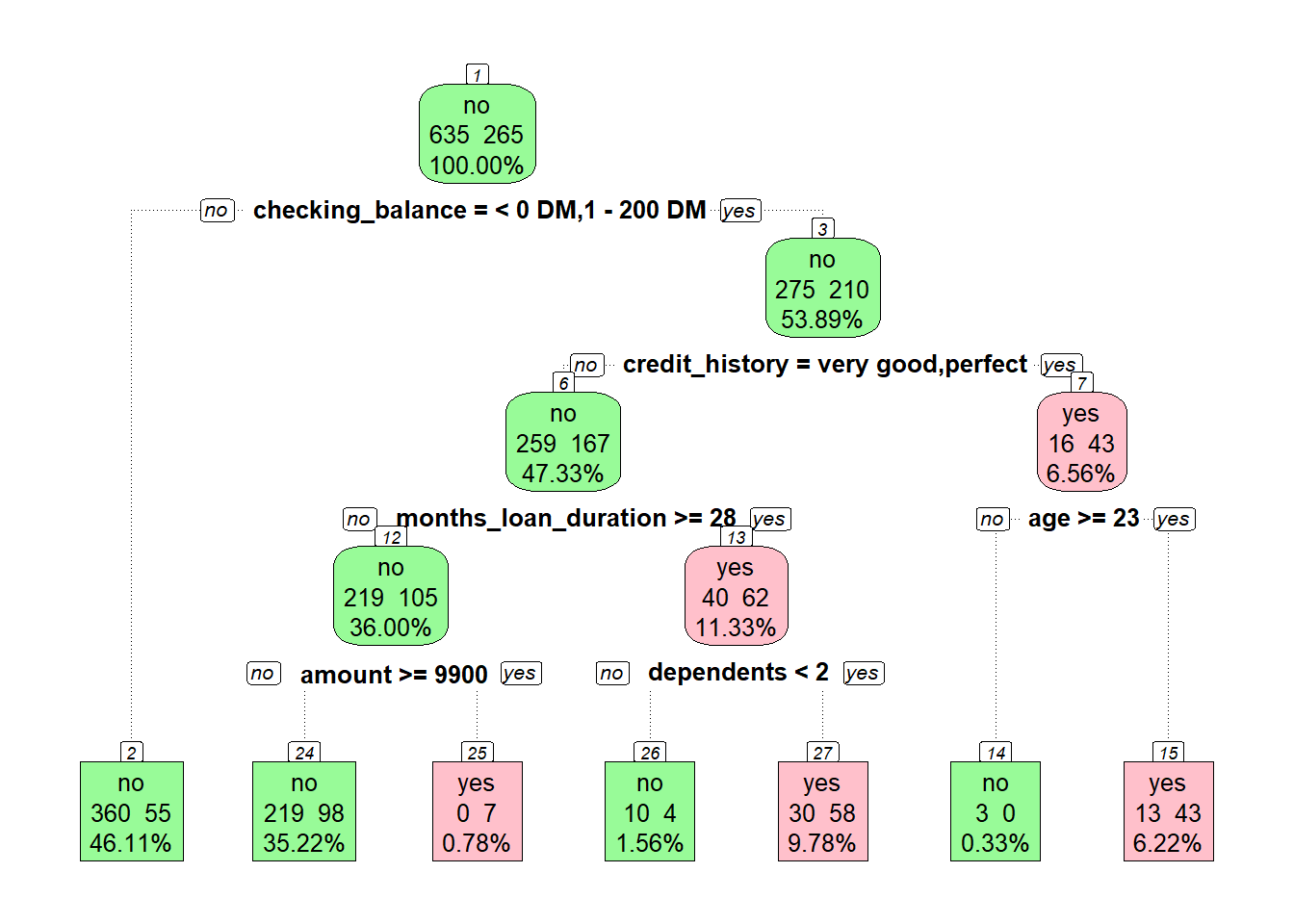

rpart.plot(tree_credit_train, yesno = 2, left=FALSE, type=2, branch.lty = 3, nn= TRUE,

box.palette = c("palegreen", "pink"), leaf.round=0, extra = 101, digits = 4)

print(tree_credit_train)n= 900

node), split, n, loss, yval, (yprob)

* denotes terminal node

1) root 900 265 no (0.7055556 0.2944444)

2) checking_balance=> 200 DM,unknown 415 55 no (0.8674699 0.1325301) *

3) checking_balance=< 0 DM,1 - 200 DM 485 210 no (0.5670103 0.4329897)

6) credit_history=critical,poor,good 426 167 no (0.6079812 0.3920188)

12) months_loan_duration< 27.5 324 105 no (0.6759259 0.3240741)

24) amount< 9899.5 317 98 no (0.6908517 0.3091483) *

25) amount>=9899.5 7 0 yes (0.0000000 1.0000000) *

13) months_loan_duration>=27.5 102 40 yes (0.3921569 0.6078431)

26) dependents>=1.5 14 4 no (0.7142857 0.2857143) *

27) dependents< 1.5 88 30 yes (0.3409091 0.6590909) *

7) credit_history=very good,perfect 59 16 yes (0.2711864 0.7288136)

14) age< 22.5 3 0 no (1.0000000 0.0000000) *

15) age>=22.5 56 13 yes (0.2321429 0.7678571) *printcp(tree_credit_train)

Classification tree:

rpart(formula = default ~ ., data = credit_train, parms = list(split = "gini"),

control = rpart.control(minsplit = 1, minbucket = 1, maxdepth = 4))

Variables actually used in tree construction:

[1] age amount checking_balance

[4] credit_history dependents months_loan_duration

Root node error: 265/900 = 0.29444

n= 900

CP nsplit rel error xerror xstd

1 0.050943 0 1.00000 1.00000 0.051599

2 0.026415 3 0.81509 0.83396 0.048726

3 0.022642 4 0.78868 0.82642 0.048577

4 0.011321 5 0.76604 0.81887 0.048425

5 0.010000 6 0.75472 0.81887 0.048425Default prediction

Because there is a 10% test set, we can test the decision tree. It’s not great. In terms of the mistake, notice that 28/35 actual defaulters were incorrectly predicted to repay; that’s terrible. Compare this to only 7/65 actual re-payers who were predicted to default.

tree_credit_pred <- predict(tree_credit_train, credit_test, type = "class")

CrossTable(credit_test$default, tree_credit_pred,

prop.chisq = FALSE, prop.c = FALSE, prop.r = FALSE,

dnn = c('actual default', 'predicted default'))

Cell Contents

|-------------------------|

| N |

| N / Table Total |

|-------------------------|

Total Observations in Table: 100

| predicted default

actual default | no | yes | Row Total |

---------------|-----------|-----------|-----------|

no | 58 | 7 | 65 |

| 0.580 | 0.070 | |

---------------|-----------|-----------|-----------|

yes | 28 | 7 | 35 |

| 0.280 | 0.070 | |

---------------|-----------|-----------|-----------|

Column Total | 86 | 14 | 100 |

---------------|-----------|-----------|-----------|

Adding a loss (aka, penalty, cost) matrix

It’s really easy to impose a penalty matrix. We will make the false negative three times more costly than a false positive. As desired, the false negatives flip with huge improvement: the updated model correctly traps 28/35 defaults with only 7/35 false negatives. But this comes with an equally huge trade-off: false positives jump from 7/65 to 27 out of 65 who are predicted to default but actually repay.

penalty_matrix <- matrix(c(0, 3, # Actual: No

1, 0), # Actual: Yes

ncol=2)

rownames(penalty_matrix) <- colnames(penalty_matrix) <- c("No", "Yes")

tree_credit_cost_train <- rpart(default ~ ., data = credit_train,

parms = list(split = "gini", loss=penalty_matrix),

control = rpart.control(minsplit = 1,

minbucket = 1,

maxdepth = 4))

tree_credit_cost_pred <- predict(tree_credit_cost_train, credit_test, type = "class")

CrossTable(credit_test$default, tree_credit_cost_pred,

prop.chisq = FALSE, prop.c = FALSE, prop.r = FALSE,

dnn = c('actual default', 'predicted default'))

Cell Contents

|-------------------------|

| N |

| N / Table Total |

|-------------------------|

Total Observations in Table: 100

| predicted default

actual default | no | yes | Row Total |

---------------|-----------|-----------|-----------|

no | 38 | 27 | 65 |

| 0.380 | 0.270 | |

---------------|-----------|-----------|-----------|

yes | 7 | 28 | 35 |

| 0.070 | 0.280 | |

---------------|-----------|-----------|-----------|

Column Total | 45 | 55 | 100 |

---------------|-----------|-----------|-----------|

Can I easily randomize?

I’m interested in the fact that decision trees have random qualities (aside from sampling variation). Below I set a different seed and switched the split algo to entropy. But the ultimate tree is the same.

# different see and switch gini to information; aka, entropy

set.seed(448)

tree_credit_train_2 <- rpart(default ~ ., data = credit_train,

parms = list(split = "information"),

control = rpart.control(minsplit = 1,

minbucket = 1,

maxdepth = 4))

rpart.plot(tree_credit_train_2, yesno = 2, left=FALSE, type=2, branch.lty = 3, nn= TRUE,

box.palette = c("palegreen", "pink"), leaf.round=0, extra = 101, digits = 4)

print(tree_credit_train_2)n= 900

node), split, n, loss, yval, (yprob)

* denotes terminal node

1) root 900 265 no (0.7055556 0.2944444)

2) checking_balance=> 200 DM,unknown 415 55 no (0.8674699 0.1325301) *

3) checking_balance=< 0 DM,1 - 200 DM 485 210 no (0.5670103 0.4329897)

6) credit_history=critical,poor,good 426 167 no (0.6079812 0.3920188)

12) months_loan_duration< 27.5 324 105 no (0.6759259 0.3240741)

24) amount< 9899.5 317 98 no (0.6908517 0.3091483) *

25) amount>=9899.5 7 0 yes (0.0000000 1.0000000) *

13) months_loan_duration>=27.5 102 40 yes (0.3921569 0.6078431)

26) dependents>=1.5 14 4 no (0.7142857 0.2857143) *

27) dependents< 1.5 88 30 yes (0.3409091 0.6590909) *

7) credit_history=very good,perfect 59 16 yes (0.2711864 0.7288136)

14) age< 22.5 3 0 no (1.0000000 0.0000000) *

15) age>=22.5 56 13 yes (0.2321429 0.7678571) *printcp(tree_credit_train_2)

Classification tree:

rpart(formula = default ~ ., data = credit_train, parms = list(split = "information"),

control = rpart.control(minsplit = 1, minbucket = 1, maxdepth = 4))

Variables actually used in tree construction:

[1] age amount checking_balance

[4] credit_history dependents months_loan_duration

Root node error: 265/900 = 0.29444

n= 900

CP nsplit rel error xerror xstd

1 0.050943 0 1.00000 1.00000 0.051599

2 0.026415 3 0.81509 0.87547 0.049518

3 0.022642 4 0.78868 0.86038 0.049236

4 0.011321 5 0.76604 0.86415 0.049307

5 0.010000 6 0.75472 0.86038 0.049236identical(tree_credit_train, tree_credit_train_2)[1] FALSEall.equal(tree_credit_train, tree_credit_train_2)[1] "Component \"call\": target, current do not match when deparsed"

[2] "Component \"cptable\": Mean relative difference: 0.04736418"

[3] "Component \"parms\": Component \"split\": Mean relative difference: 1"

[4] "Component \"splits\": Attributes: < Component \"dimnames\": Component 1: 4 string mismatches >"

[5] "Component \"splits\": Mean relative difference: 5.545437"

[6] "Component \"csplit\": Attributes: < Component \"dim\": Mean relative difference: 0.04761905 >"

[7] "Component \"csplit\": Numeric: lengths (126, 120) differ"

[8] "Component \"variable.importance\": Names: 2 string mismatches"

[9] "Component \"variable.importance\": Mean relative difference: 0.1894674"